It’s the time of the year that the annual renewal of some of my family insurance policies is needed. While organizing my family’s insurance policies, I thought that since I’ve discussed various insurance topics, why not share the principles and strategies of my family insurance planning directly, similar to what Morgan Housel’s confession in the last chapter of the book The Psychology of Money, which are practical and convincing advices.

Determining Priorities

Through my personal experiences while learning from insurance agents and doing my own research, I have distilled three basic principles:

- Medical insurance is the most fundamental protection

- Prioritize safeguarding the family’s income earners

- Buy term and invest the rest

Detail about the principles is summarized in the table below. I have also written a blog post on how to buy insurance in Singapore, based on the principles the Singaporean government follows when planning insurance for its residents – hospitalization insurance at birth, life insurance at the beginning of one’s career, long-term care insurance starting at the age of 30, left critical illness and accident insurance being optional. Our own insurance should follow a similar priority.

Other types of insurance can be determined based on the family’s situation:

- Car insurance

- Home insurance

- Maid insurance

- Travel insurance

- Pregnancy insurance

Identifying Gaps - Using a Coverage Matrix Form

Based on the priorities mentioned above, I created an insurance coverage matrix (click to download). I filled in the corresponding types of coverage and specific insurance plans, including premiums and coverage amounts. This helps check for any gaps in coverage and ensures that premiums and coverage amounts are within reasonable ranges. The yellow highlights indicate that CPF can be used to pay (part or all of) the premiums.

I also maintain a list of all our insurance policies, allowing for quick access to policy details, payment deadlines, and more. The format of this table is based on my insurance agent’s recommendation, as responsible agents should help clients manage their policies. I manage all the policies myself because our insurance configurations change over time and involve different insurance agents. I haven’t found a single financial advisor under a commission-based system who can manage all my policies. However, this process of organizing and learning is a rewarding journey to me.

This year, I took the opportunity to adjust my family’s whole life insurance by removing all critical illness riders. Considering the sunk costs if I were to surrender the whole life policy and the potential 3% to 4% returns in the long run, I decided to keep it and treat it as a low-risk investment.

Since my husband is currently the sole borrower for our mortgage, I advised him to add a term life insurance policy with a coverage period up to age 65. He had just resolved an issue with the previous insurer, which mistakenly duplicated a term policy (Here is the story). Surprisingly, the new policy with coverage up to age 65 was cheaper than the previous policy covering up to age 60. As life expectancy increases and insurance penetration rises, insurance companies lower their costs, term life insurance premiums have been consistently decreasing.

My husband is an ISTJ, a workaholic, and has always believed that his career will last long, with no plans for early retirement. I, on the other hand, am an INFP, naturally inclined towards a relaxed lifestyle, preparing for a gradual decrease in income and early retirement. In the long run, my husband will become more of the family’s main income earners, so his life insurance coverage is higher. Due to a family history of cancer, I added a cancer-specific term policy. We also purchased basic accident and hospitalization insurance for our child and parents. I added a critical illness policy for our child, which turned out to be a fortunate decision, as it was in place before he had recurrence Kawasaki disease. The premiums for our parents’ hospitalization insurance are relatively high, but they each have about $1600+ in my Medisave to cover them.

How much do these premiums cost? Excluding the portion covered by CPF, our monthly insurance expenses are around $1400. I haven’t factored in the cash value of the whole life insurance, as I consider it a low-risk investment. Hospitalization insurance for our parents takes up a significant portion, but I believe it’s necessary. For a small family of three, monthly insurance coverage of under $1000 would be more than sufficient.

The Coverage Matrix was a genuine idea by myself and I love how it had helped me to clear my mind about family insurance planning. Maintaining the spreadsheet is tedious for me, so I move everything to a web app. Try the insurance planner here

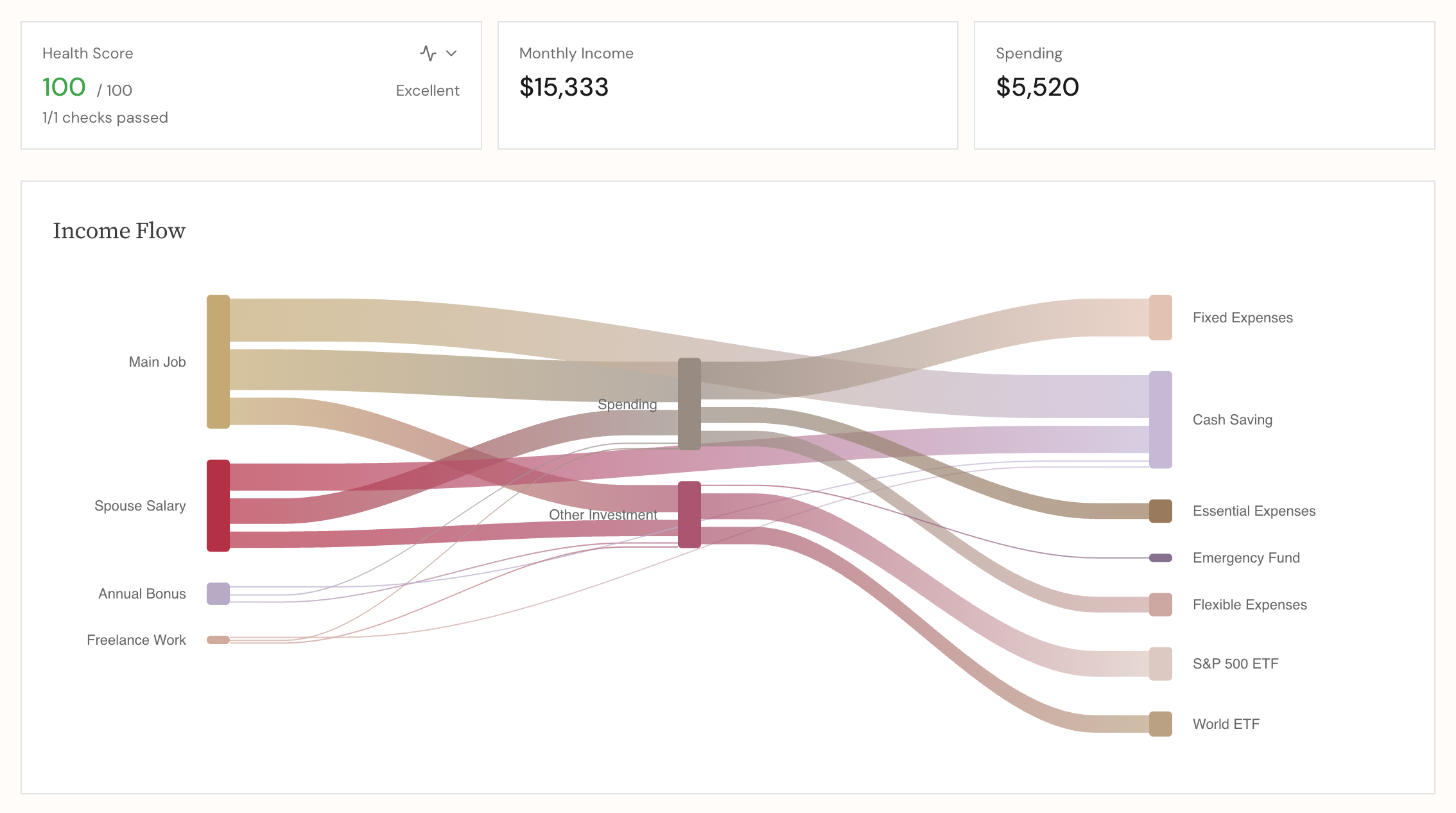

My Financial Planner

Track your portfolio, budget, and income flow with interactive visualizations. Plan your path to financial independence.

Try It Now

My Opinions

Due to my personal experiences with care giving to family member in severe medical condition, my family is somewhat over-insured in terms of protection insurance, and some of our insurance configurations may not offer the best value for money. While it’s rational to aim for ‘minimal cost for adequate coverage’ when it comes to insurance allocation, implementing it can be challenging. Here are some of the challenges I’ve identified:

- Insurance is a long-term commitment with significant sunk costs.

I believe many people made mistakes in insurance planning when they were young due to a lack of financial literacy, and some insurance products come with high penalties for early termination. For example, savings insurance policies have hefty surrender charges, and if one purchases hospitalization insurance when young and later develops pre-existing conditions, switching insurance companies can be risky. The high costs of switching products are due in part to the commission-driven sales culture prevalent in the insurance industry. Many so-called financial advisors do not provide proper guidance and may not even guarantee basic after-sales service. The government has been making efforts to improve financial literacy among the public (e.g., CompareFirst, MoneySense, CPF). This is one of the main reasons that I started to write blog posts spreading wealth management ideas, as only when overall financial literacy in society improves can the insurance industry become more regulated.

- The human factor in insurance is challenging to quantify.

While I appreciate the efficiency and transparency of digital platforms, I’ve learned the importance of service during the insurance claim process. After acquiring some financial knowledge and finding a relatively reliable insurance agent, I established a good working relationship with her. She doesn’t need to push policies on me because I understand the necessity of insurance, and I can honestly express my opinions about any unreasonable insurance configurations. A good insurance agent can also provide excellent service and consultation on various apesct of life other than insurances. When considering insurance costs, it’s challenging to put a price on the “human” factor, especially in an industry that operates on a commission-based sales system.

- Life is full of uncertainty.

Though we can follow some guidelines’ suggestion to allocate specific coverage amounts for life and critical illness insurance based on income, life is constantly changing. Our income, family situation, and unforeseen surprises or accidents are hard to predict. For instance, my family’s income has increased noticeably in recent years, and due to the pandemic, we’ve transitioned to a three-generation household. Our previous insurance coverage was clearly inadequate. Additionally, because of recurring health issues in our family, I have placed more emotional reliance on health-related coverage. Therefore, I allocated an extra budget for a comprehensive but relatively expensive critical illness insurance.

Despite the above points, I believe in some fundamental principles that should guide our approach to insurance planning from the start:

Budget and Need-Based Approach: When it comes to protection insurance (such as life and critical illness insurance), focus on your budget and needs rather than obsessing over return rates or probabilities. Your insurance coverage should align with your financial capacity and provide the necessary protection.

Separate Protection and Investment: Keep your insurance and investment goals separate. While insurance provides protection, investments serve as a means to grow your wealth. Compare investment linked insurance products with other investment and savings options to make informed decisions. I’ve written an article about breaking down Investment-Linked Plan (ILPs). The specific numbers may not be accurate and conclusions may vary based on personal preferences, I believe I have made an effort to convey a balanced and objective perspective on investment-linked insurance products.