I’ve decided to handle my family finances on my own. The main reasons are:

- Financial decisions are built upon life decisions, and I need to be completely honest with a financial advisor for them to help us make the most reasonable plan. However, for me it’s difficult to fully open up about my personal dreams and family plans to someone else without a deep trust.

- We need insurance agencies to handle policies, real estate agencies for property transactions, banks for loans, and law firms for wills. Without anyone of these, financial planning isn’t complete. I feel that Singapore society hasn’t developed to the point where ordinary income earning (non high-net-worth) families can easily access professional financial planning services that manage all-in-one.

- Ordinary families don’t have large sums of wealth to ‘manage’. Through books, MOOCs, and media platforms, one can obtain sufficient financial knowledge, and with retail financial investment products and some affordable professional services, one can meet their own financial needs.

Now, let me explain how I go about it by start with the following three questions:

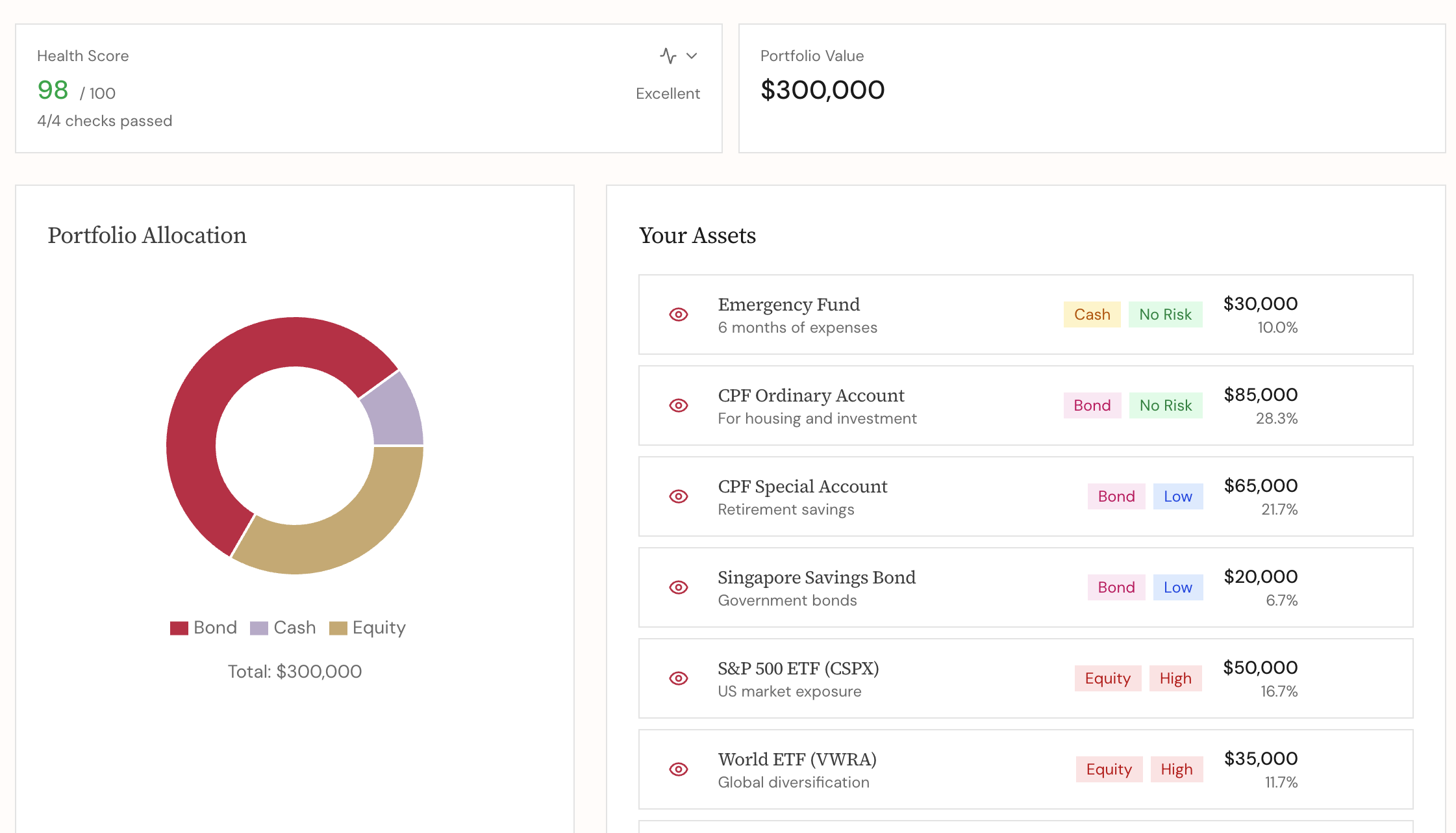

✍🏻 How much assets do we have: Calculate the family’s Net Worth

List the family’s net worth and see if it’s healthy:

- For instance, do we have enough emergency funds?

- Is the proportion of our primary residence assets reasonable? Although a primary residence is an asset, it doesn’t generate positive cash flow and shouldn’t make up a high percentage of total assets.

- Are savings and investments diversified, and is the risk balanced?

This can be recorded quarterly to track changes in family net worth—hopefully, it steadily increases 📈.

Net Worth Tracking Form Sample(download)

Regarding net worth, we can also refer to Singapore’s national data (reference):

- Singaporean households have a relatively balanced proportion of housing and other financial assets.

- In the distribution of financial assets, cash savings and CPF (Central Provident Fund) account for the majority. Among investment-type financial assets, life insurance has the highest proportion. I can understand that Singaporean households generally have a low risk appetite, relying mostly on managed and insurance-type investment products.

- Singaporean households have a debt-to-asset ratio of around 12%, which is very healthy. Of course, it varies with age, and for young individuals in the income growth and wealth accumulation phase, a slightly higher mortgage ratio is reasonable. If we calculate the proportion of property and investment-type financial assets (excluding cash savings and CPF), it’s over 70%, indicating that Singaporean households still primarily invest in real estate.

The above data represents overall net worth statistics with a strong age bias. Older individuals have accumulated assets, contributing significantly to the total, but their risk appetite is low as they approach retirement or are already retired. Therefore, the overall data reflects a conservative investment allocation for middle-aged and older individuals nearing retirement. It may not be a complete reference for young families who are still in the asset accumulation phase, but similar analyses are crucial.

I believe there are two pitfalls to be wary of:

- Investing too conservatively.

- Having an excessively high proportion of real estate investments.

Being overly conservative in investments (e.g., 3-4% bond investments) show limits in asset appreciation or inflation protection. If low-risk investments significantly dominate the balance sheet, be cautious.

This year, thanks to changing homes and reconfiguring insurance, I have had interactions with a few real estate agencies and insurance agencies. An interesting discovery is that when real estate brokers agencies affordability for us initially, they base it on the family’s maximum loan amount. My insurance agent however, timely reminded me that property prices are at the all-time high and recommended investment products. There are vested interests for them, of course, and only when we know our own debt-to-asset ratio, understand our financial goals, and risk preferences, can we make better choices. I can’t definitively answer whether investing in real estate or the stock market is more advantageous. I endorse the Chinese tradition of investing in real estate, but my attitude is balanced: strive for optimal ratio.

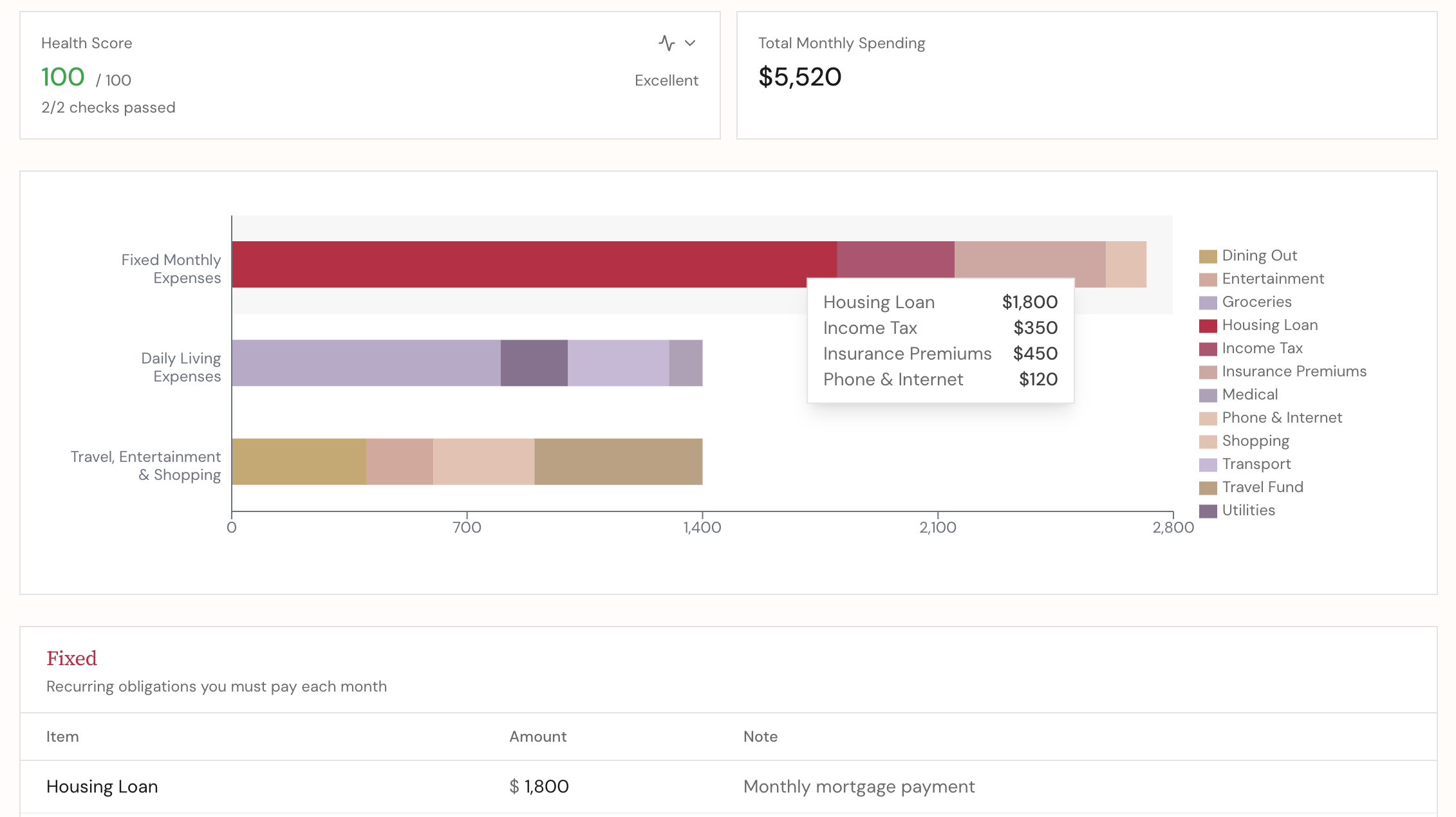

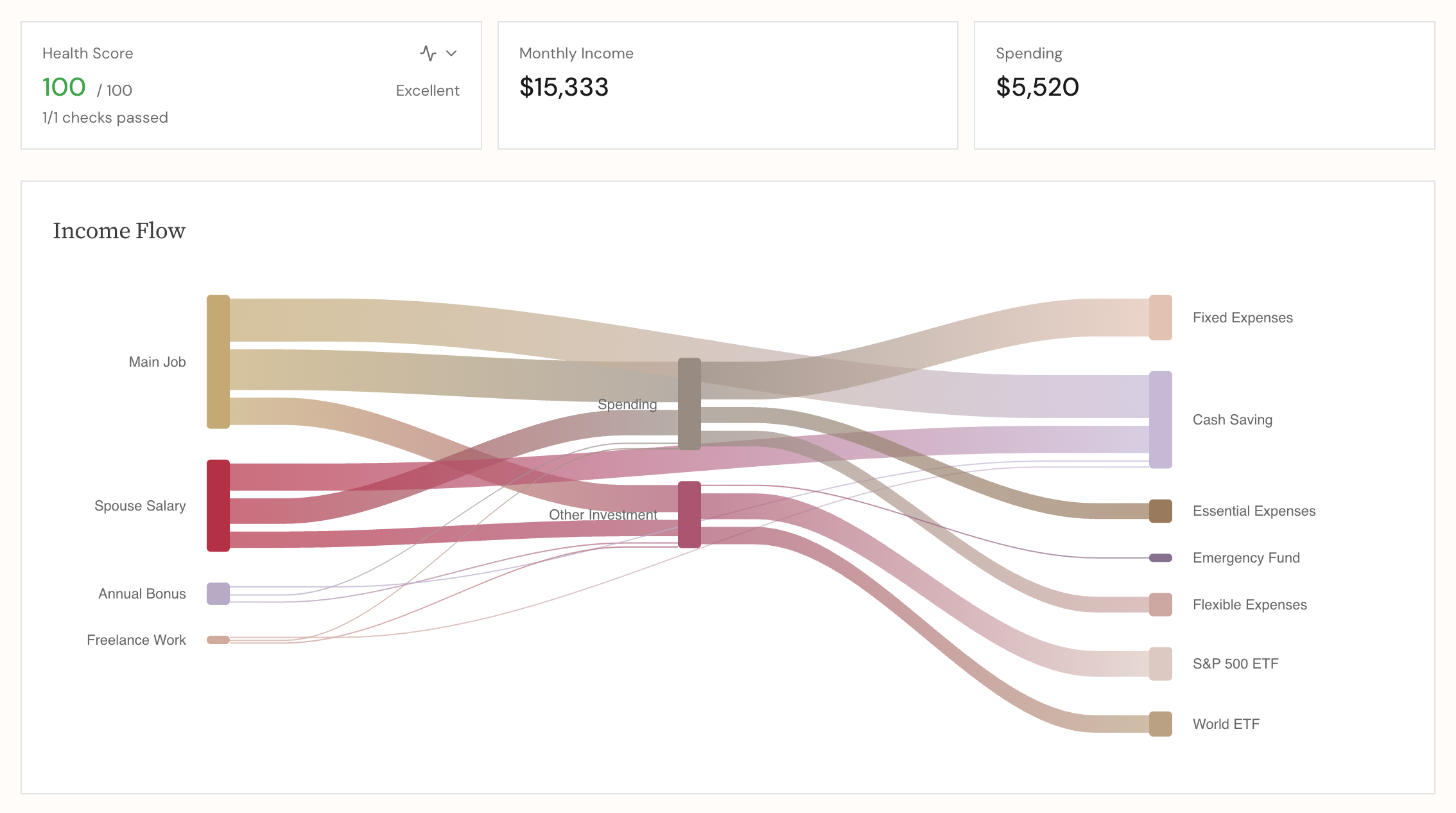

✍🏻 How much do we earn, spend, and save: Calculate family cash flow and expenses, do budgeting

Recording is the first step in planning. Knowing the specific numbers of income and expenses allows for reasonable planning. I divide budgeting into several parts:

- Savings and investments.

- Fixed expenses: insurance, mortgage, taxes, property expenses, children’s tuition, etc.

- Essential expenses: transportation, groceries, utilities, etc.

- Flexible expenses: non-essential consumption, travel, etc.

By automating regular investments before spending, I ensure a savings rate. Fixed expenses are essential and difficult to reduce. If a major financial crisis requires a reduction in fixed expenses, it may involve significant lifestyle changes such as downgrading housing. However, basic expenses and flexible expenses can be controlled through moderate consumption downgrades, sacrificing some quality of life but not disrupting the current lifestyle abruptly. In actual life, because both my husband and I have relatively good spending habits (he is naturally frugal, and I am still working on this), we make rough estimates without meticulously tracking every cent.

I have been using spreadsheet to do budgeting and income distribution planning. Then I developed my own financial planner tool that can do the same thing with nicer and richer experience - budgeting and income planner

My Financial Planner

Track your portfolio, budget, and income flow with interactive visualizations. Plan your path to financial independence.

Try It Now

The Singapore government conducts surveys to present the national household expenditure data every five years, which can be used to compare one’s spending with the average. The last statistics were from 2017/18, adjusted for a high inflation rate of 3% annually. The new five-year statistics should be available soon for further reference. Note that housing expenses are excluded from the expenditure statistics.

It can be observed that as income increases, the proportion of spending decreases, leaving more money for investment and savings. Good spending habits, avoiding excessive upgrades and even engaging in occasional spending downgrades, are crucial for wealth accumulation.

✍🏻 What are our life plans: Goals determine investment choices

Earning and saving money are about improving one’s life and the lives of one’s family, both now and in the future. I have always believed that financial planning is not just about saving and making money work for you; it’s about realizing life goals, with money being just a tool. After some detours and tuition fees paid in the form of mistakes, I’ve simplified my main financial strategy:

- Avoiding unhealth debt: Car loans, credit card installment loans, etc. I only use one credit card for daily expenses.

- Conservative investment in the primary residence: Not maxing out the loan amount for primary residential property, and ensuring that the monthly mortgage payment is below 20% of family income.

- Understanding my risk preference and investing in low-cost, low-maintenance assets.

- Insurance: Allocating insurance primarily for protection against unexpected expenses beyond life plans.

- Short-term savings: Saving accounts, fixed deposits, Singapore Savings Bonds (SSB), T-bills, Money Market Funds.

- Long-term investments: Central Provident Fund Special Account (CPF SA) Top-Up, Index ETF.

I will continue share money philosophy and investment strategies in my blog. As for life and dreams, I also hope to continue writing about nice pieces of memory of my life.

Reference

Read More

How to Buy Health Insurance and What Coverage Should Last a Lifetime

My medical and critical illness insurance strategy: why I prefer term coverage over whole life, and what elderly truly need for lifelong protection.

How to Buy Insurance as Home Owners

Understanding mandatory fire and mortgage insurance for home owners, plus optional home insurance to protect personal property and belongings.