Let’s get this out of the way — I’m not directly comparing IUL (Indexed Universal Life Insurance) here, because as an insurance product, IUL has its own unique purposes: legacy planning, tax advantages, asset protection, and so on. These features make it difficult to draw a fair comparison with pure investment strategies.

Instead, what I’m comparing here is just the investment logic behind downside-protected strategies.

☂️ Investment Logic Behind Floors and Caps

The floor-and-cap model used in IUL mirrors a downside-protected portfolio. Here’s how that’s defined:

❝ Downside protection refers to techniques used in investing to mitigate or prevent a decline in asset value. Common tools include stop-loss orders, options contracts, and other hedging instruments designed to limit losses in individual positions or portfolios. ❞

In short, these strategies seek to provide a safety net — limiting downside risk, but often capping upside potential.

✍🏻 Historical Backtesting (Excluding Fees)

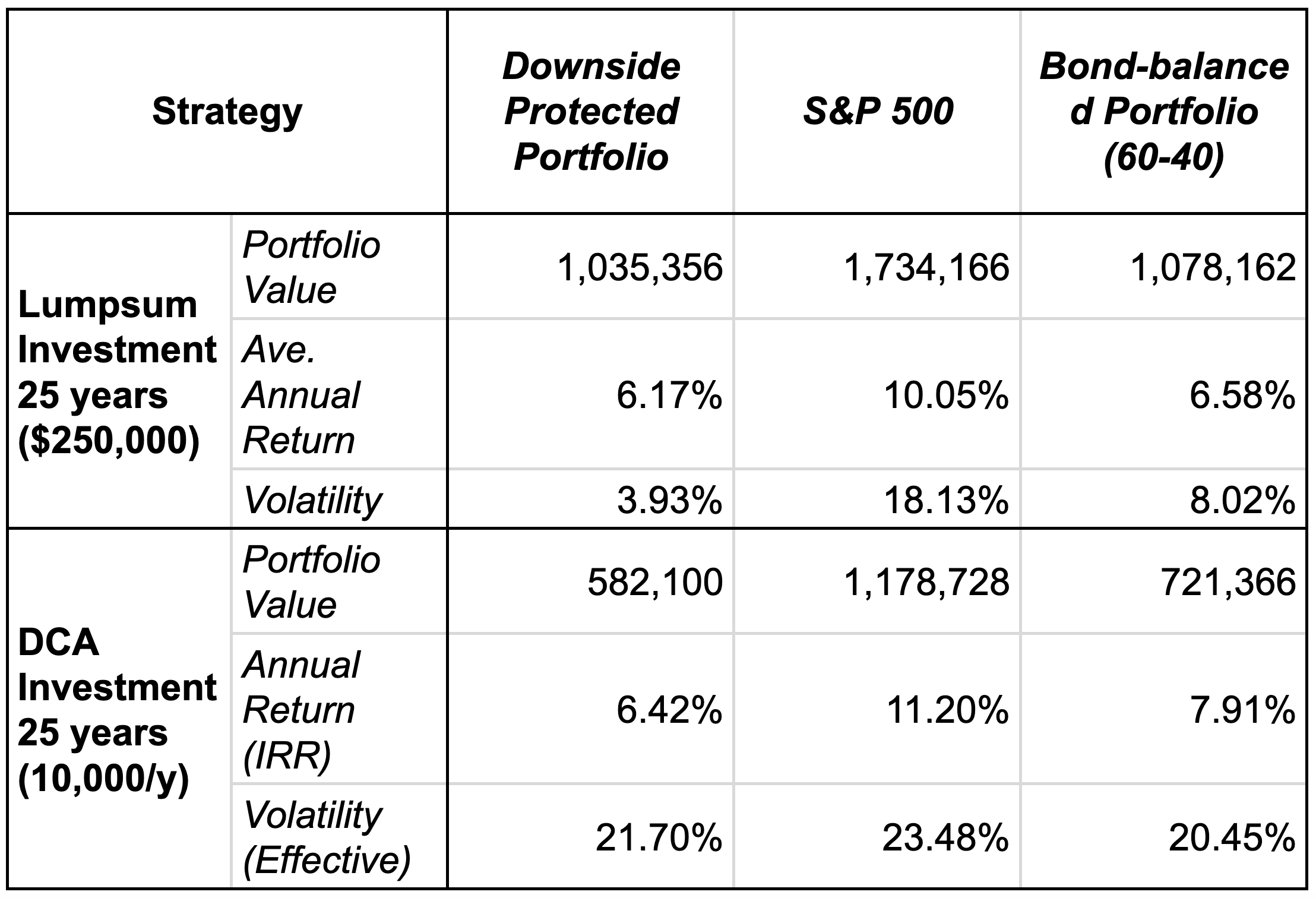

Let’s look at three basic investment strategies (fee-free for simplicity):

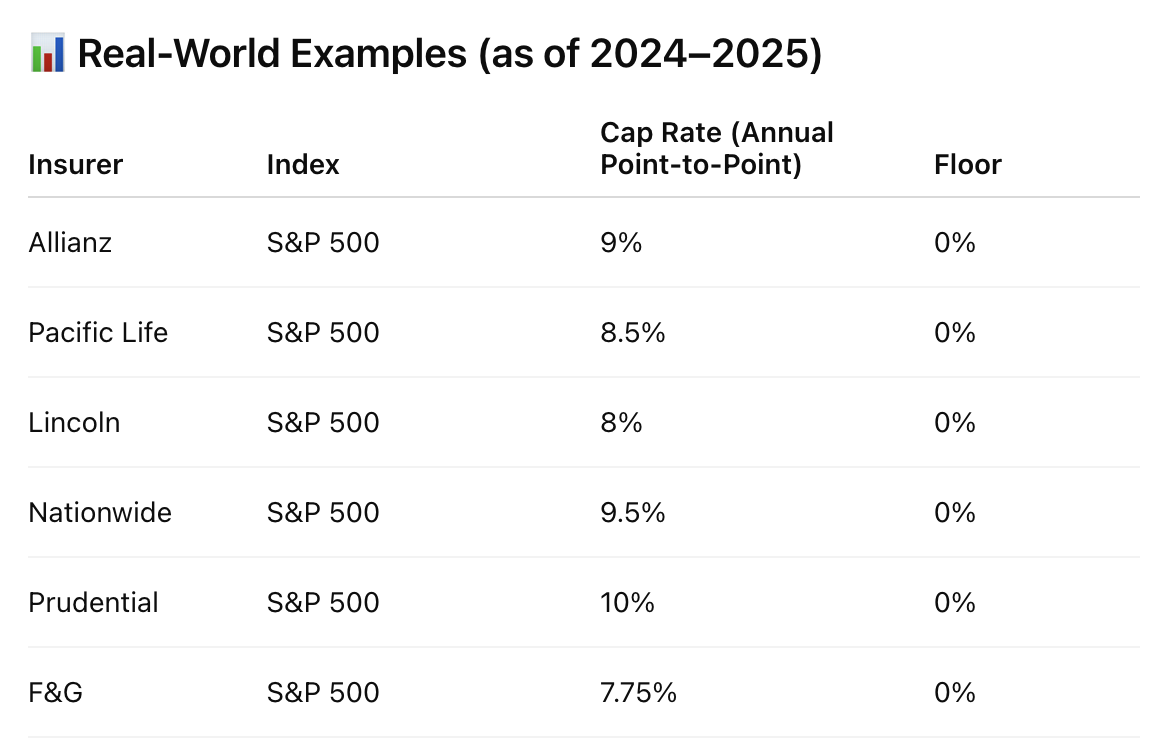

❶ Downside-protected strategy: 0% floor and 9% cap (data based on available option pricing — see below)

❷ Direct investment in the index: Riding full market volatility

❸ Low-volatility alternative: A 40/60 stock-bond portfolio, assuming a fixed 4% bond yield

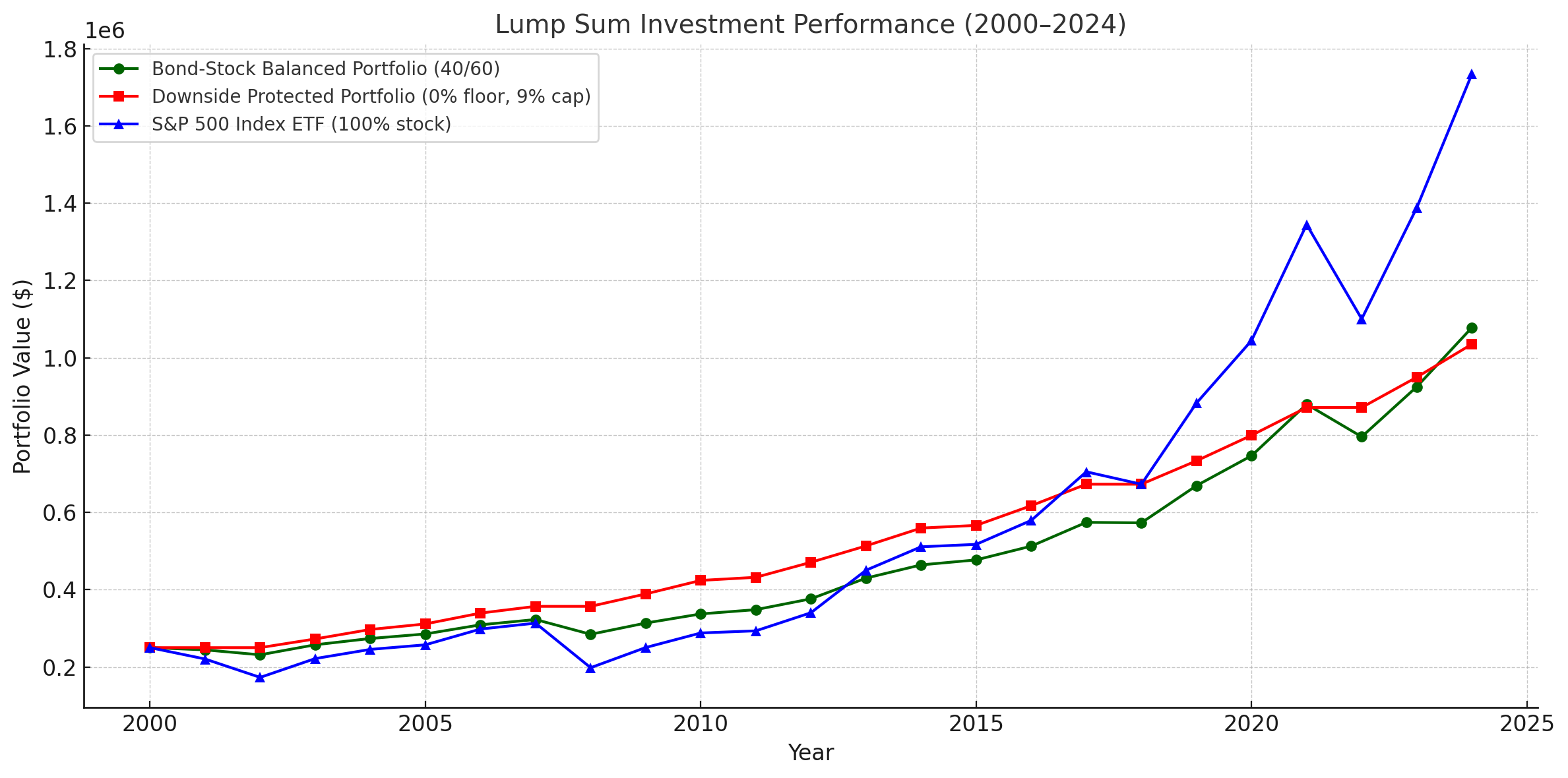

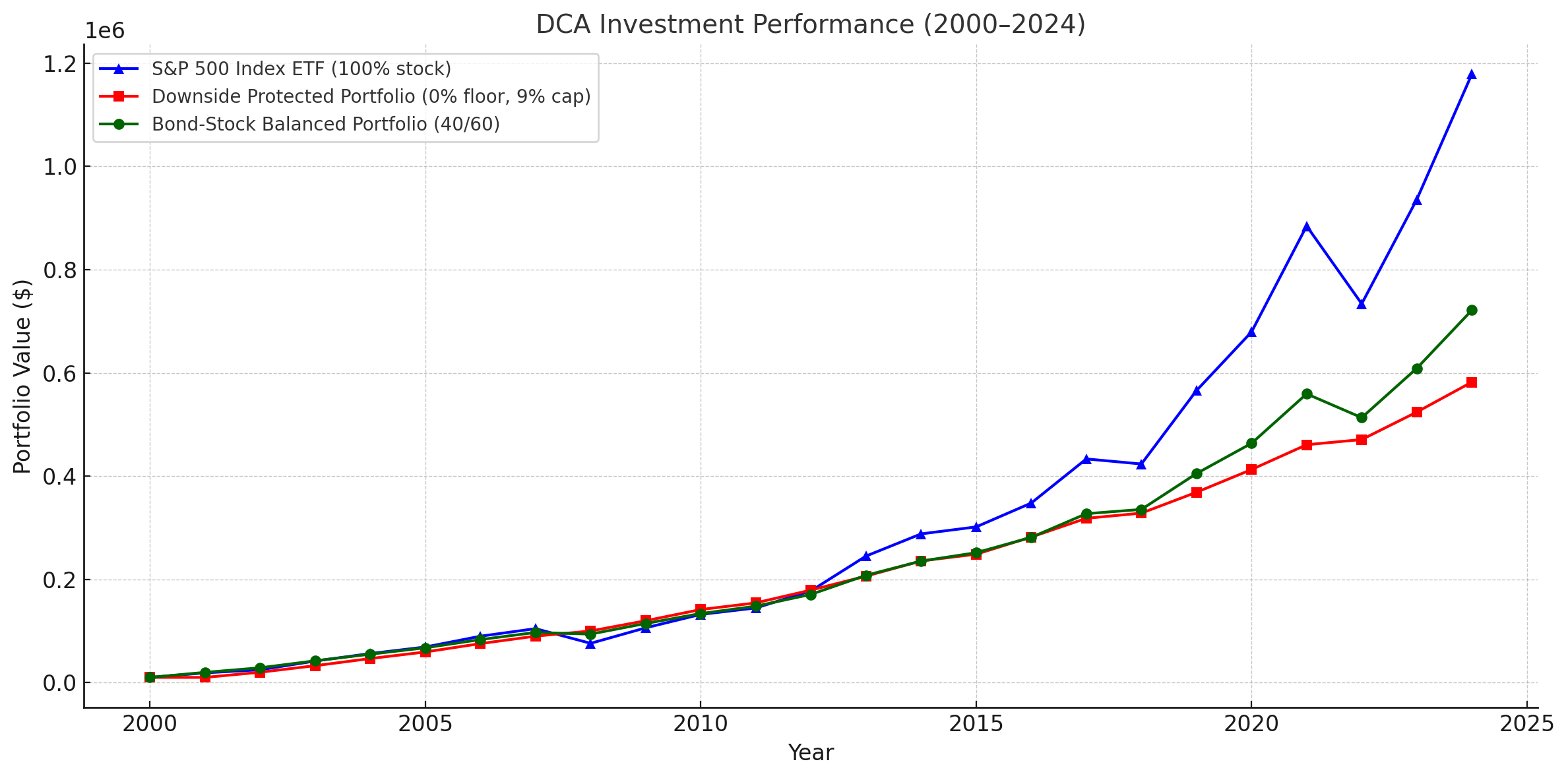

I ran a backtest comparing both lump-sum investing and dollar-cost averaging (DCA) over a 25-year period using S&P 500 index data. See Figures 3, 4, and 5 for detailed outcomes.

(Note: This comparison does not include fees. Downside-protected portfolios generally involve options or structured derivatives and would logically have higher fees than passive index funds.)

Calculation Script (Click to Expand)

import yfinance as yf

import pandas as pd

import numpy as np

import numpy_financial as npf

import matplotlib.pyplot as plt

# Parameters

ticker = 'SPY'

start_year = 2000

end_year = 2024

# Fetch SPY historical data

data = yf.download(ticker, start=f'{start_year}-01-01', end=f'{end_year+1}-01-01')

data = data['Close']['SPY'].resample('Y').last() # Year-end adjusted close prices

def sp_500(init_amount, annual_investment):

# Initialize tracking

units_owned = init_amount / data[0]

total_invested = init_amount

portfolio_values = []

prices = []

for price in data:

units_bought = annual_investment / price

units_owned += units_bought

total_invested += annual_investment

portfolio_value = units_owned * price

prices.append(price)

portfolio_values.append(portfolio_value)

cash_flows = [-annual_investment] * 25

cash_flows[-1] += portfolio_values[-1] # Final value added in last year

# Calculate returns

irr = npf.irr(cash_flows)

returns = pd.Series(portfolio_values).pct_change().dropna()

average_return = returns.mean() if math.isnan(irr) else irr

volatility = returns.std()

# Build result DataFrame

df = pd.DataFrame({

'Year': list(range(start_year, start_year + len(prices))),

'SPY Price': prices,

'Portfolio Value': portfolio_values

})

# Print results

print(f"\nSummary for S&P 500 with {init_amount} initial investment and {annual_investment} annual investment:")

print(f"Total Invested: ${total_invested:,.2f}")

print(f"Final Portfolio Value: ${portfolio_values[-1]:,.2f}")

print(f"Average Annual Return: {average_return:.2%}")

print(f"Annual Volatility: {volatility:.2%}")

return df

def downside_protected(init_amount, annual_investment):

cap = 0.09

floor = 0.00

# Calculate actual yearly returns

returns = data.pct_change().dropna()

# Apply IUL-style return constraints

capped_returns = returns.clip(lower=floor, upper=cap)

# Simulate portfolio with yearly investment and capped returns

portfolio_values = []

current_value = init_amount

total_invested = current_value

for r in capped_returns:

current_value = (current_value + annual_investment) * (1 + r)

total_invested += annual_investment

portfolio_values.append(current_value)

# Add first year manually (no return applied yet)

portfolio_values = [init_amount + annual_investment] + portfolio_values

total_invested += annual_investment

cash_flows = [-annual_investment] * 25

cash_flows[-1] += portfolio_values[-1] # Final value added in last year

# Build DataFrame

df = pd.DataFrame({

'Year': list(range(start_year, end_year + 1)),

'Capped Return': [0.0] + list(capped_returns),

'Portfolio Value': portfolio_values

})

# Calculate stats

irr = npf.irr(cash_flows)

final_value = portfolio_values[-1]

avg_return = capped_returns.mean() if math.isnan(irr) else irr

volatility = pd.Series(portfolio_values).pct_change().std() if annual_investment > 0 else capped_returns.std()

# Print results

print(f"\nSummary for downside protected portfolio with {init_amount} initial investment and {annual_investment} annual investment:")

print(f"Total Invested: ${total_invested:,.2f}")

print(f"Final Portfolio Value: ${final_value:,.2f}")

print(f"Average Annual Return (Effective): {avg_return:.2%}")

print(f"Volatility (Effective): {volatility:.2%}")

return df

def bond_balanced(init_amount, annual_investment):

stock_ratio = 0.4

bond_ratio = 1 - stock_ratio

bond_return = 0.04 # 4% fixed annual return

# Calculate SPY annual returns

stock_returns = data.pct_change().dropna()

# Initialize portfolio values

total_invested = init_amount

stock_value = total_invested * stock_ratio

bond_value = total_invested * bond_ratio

portfolio_values = []

# Simulate year by year

years = list(range(start_year, end_year + 1))

portfolio_values.append(init_amount + annual_investment) # Year 2000 (first investment)

stock_value += annual_investment * stock_ratio

bond_value += annual_investment * bond_ratio

total_invested += annual_investment

for r in stock_returns:

# Apply returns

stock_value *= (1 + r)

bond_value *= (1 + bond_return)

# Add new investment

stock_value += annual_investment * stock_ratio

bond_value += annual_investment * bond_ratio

total_invested += annual_investment

total_portfolio = stock_value + bond_value

portfolio_values.append(total_portfolio)

cash_flows = [-annual_investment] * 25

cash_flows[-1] += portfolio_values[-1] # Final value added in last year

# Calculate stats

irr = npf.irr(cash_flows)

returns = pd.Series(portfolio_values).pct_change().dropna()

average_return = returns.mean()

volatility = returns.std() if math.isnan(irr) else irr

# Build DataFrame

df = pd.DataFrame({

'Year': years,

'Portfolio Value': portfolio_values

})

# Output

print("\nSummary:")

print(f"Total Invested: ${total_invested:,.2f}")

print(f"Final Portfolio Value: ${portfolio_values[-1]:,.2f}")

print(f"Average Annual Return: {average_return:.2%}")

print(f"Annual Volatility: {volatility:.2%}")

return df

def plog_data(title, df_sp500, df_downside_protected, df_bond_balanced):

plt.figure(figsize=(10, 6))

plt.title(title)

plt.xlabel("Year")

plt.ylabel("Portfolio Value ($)")

plt.grid(True)

plt.tight_layout()

plt.plot(df_sp500['Year'], df_sp500['Portfolio Value'], marker='o', label='S&P 500')

plt.plot(df_downside_protected['Year'], df_downside_protected['Portfolio Value'], marker='x', label='Downside Protected')

plt.plot(df_bond_balanced['Year'], df_bond_balanced['Portfolio Value'], marker='s', label='Bond Balanced')

plt.legend(loc="upper left")

plt.show()

# Calculate and Plot Lumpsum investment strategy:

plog_data("Lumpsum Investment Performance (2000-2024)",

sp_500(250_000, 0),

downside_protected(250_000, 0),

bond_balanced(250_000, 0))

# Calculate and Plot DCA investment strategy:

plog_data("DCA Investment Performance (2000-2024)",

sp_500(0, 10_000),

downside_protected(0, 10_000),

bond_balanced(0, 10_000))

💭 Key Takeaways

The basic principle still holds: higher returns usually come with higher volatility. If you want to avoid market risk, you’re likely giving up part of the potential upside.

For lump-sum investors, downside-protected portfolios can offer real advantages during turbulent markets. They reduce volatility and ensure no capital loss — which can make sense for those with short time horizons or near-term liquidity needs.

For DCA investors, however, these strategies lose their shine. When the market dips, DCA lets you buy at lower prices — something a downside-protected portfolio can’t capitalize on due to its capped upside. In this case, volatility isn’t necessarily bad. These portfolios often exhibit similar volatility to the index itself, and even more than a balanced stock-bond portfolio — but with significantly lower long-term returns.

Looking at rolling one-year returns of the S&P 500, the most frequent annual return range is 10% to 20% — already above the annual return cap in most downside-protected ETFs or strategies. The opportunity cost of that cap is significant, and compounded over time, it becomes hard to ignore. Missing out on just 5–10% annually can lead to 27% to 61% less in total returns over just five years.

Disclaimer: This article reflects personal views and does not constitute financial advice.

Read More

Dismantle one 101 Investment-Linked Plan (ILP)

A transparent, unbiased comparision of 101 ILP (FWD), Robo Advisor (Endowus) and direct ETF investment, with actual numbers and python scripts.

Common Investment Misconceptions

Four common investment mistakes: being overly conservative, single investment channels, over-focusing on passive income early, and chasing growth in retirement.