Cancer Treatment’s Insurance Coverage and Insurance Agent’s Negligence

After a year of targeted therapy, my mother’s condition remained stable (This article is about the cancer diagnose and treatment cost). However, in April 2024, during an insurance claim process, the insurance company missed part of the reimbursement.

I called my insurance agent to check, and he told me:

“Cancer treatment reimbursement only covers expenses incurred within one year of hospitalisation.”

This statement shocked me, as it completely contradicted my previous understanding of the IP insurance policy. If this were true, our financial burden for ongoing treatment would increase significantly, potentially forcing us to reconsider the current treatment plan.

🏥 Seeking clarification

Doubting his response, I searched online for information and consulted other insurance agents, but none could provide a 100% definitive answer.

Some kind-hearted cancer patients online shared their experiences and suggested asking the clinic’s administrative staff, as they handle e-filing for insurance claims daily and are more experienced with practical claim processes.

During my mother’s routine follow-up, I took the opportunity to consult the front desk nurse at a cancer treatment clinic in Mount Elizabeth. She patiently went through my invoices item by item and provided a clear explanation:

- E-filing is not available for foreigners. This aligned with what I already suspected, as foreigners also cannot e-file hospital surgery bills.

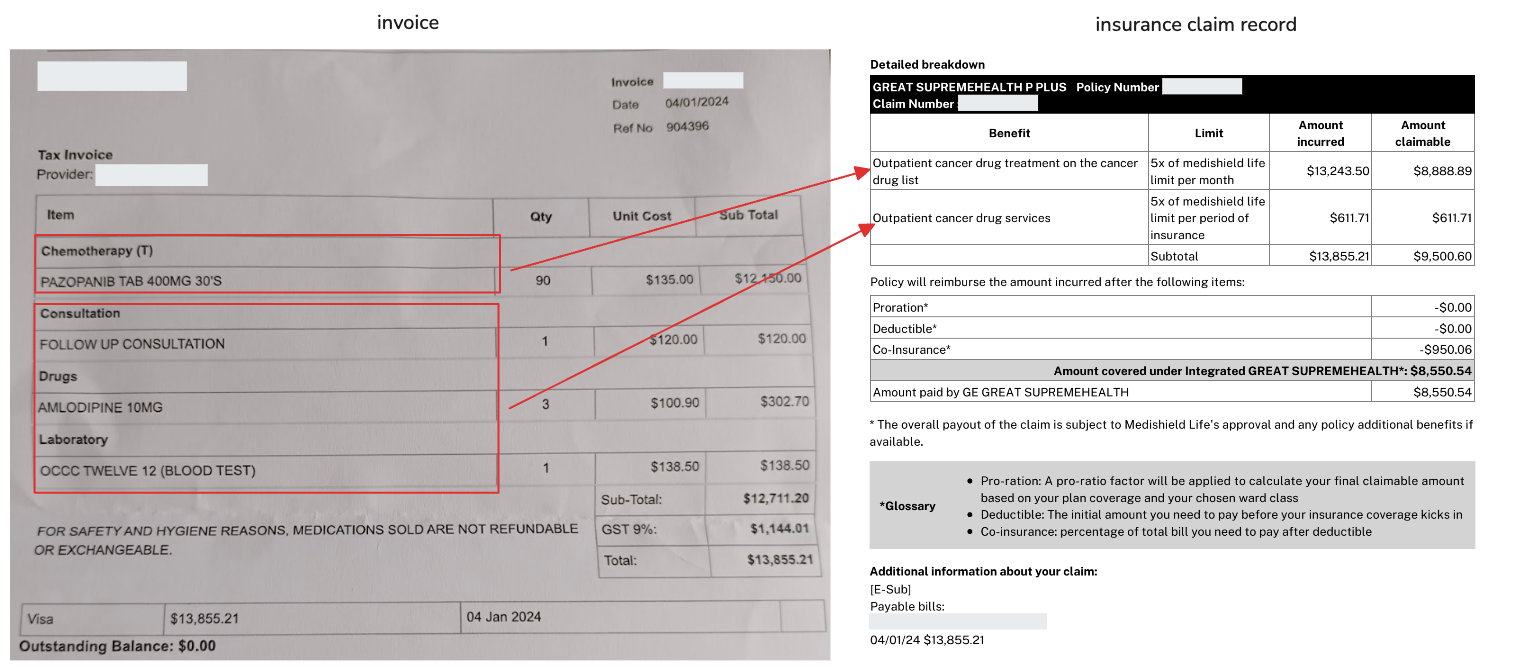

- Breakdown of claimable expenses. This explanation matched my own understanding of the policy and contradicted the incorrect information from my insurance agent:

Chemotherapy drugs listed under the Cancer Drug List (CDL) are covered under the outpatient cancer drug treatment category, with a monthly reimbursement limit based on a multiplier of the government’s CDL cap. For example, under the new policy, Our Private + Rider IP covers 18× the standard government limit, with a 5% co-payment.

Consultations, scans, and blood tests are reimbursed under outpatient cancer drug services, which have an annual reimbursement cap. Our insurance does not have an annual cap, but still requires a 5% co-payment.

🏥 Escalating the issue with the insurance agent

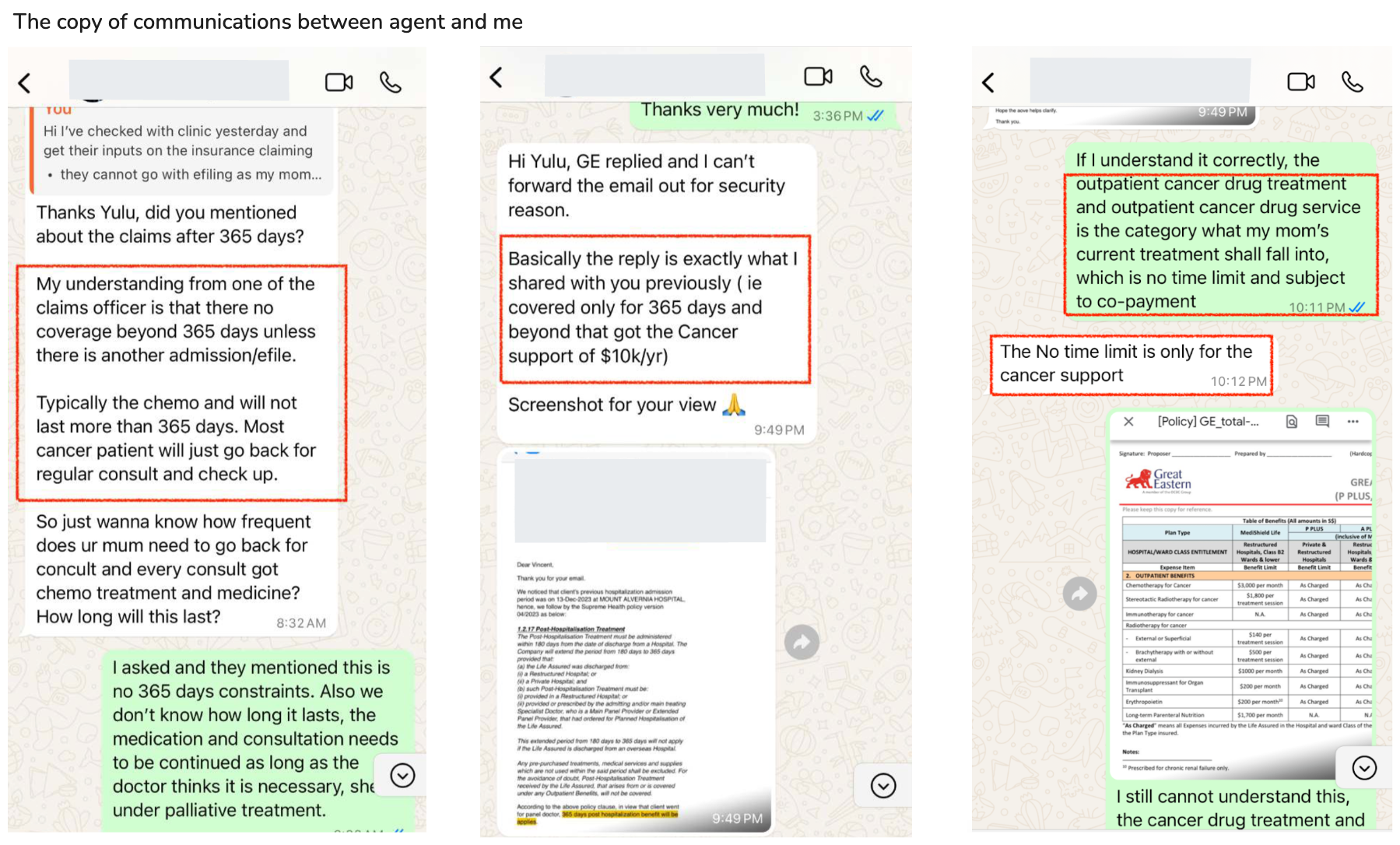

I confronted my agent again, but he insisted:

“Treatment beyond one year of hospitalisation is not claimable.”

I repeatedly asked him to verify this, even providing hospital invoices and excerpts from the insurance policy for reference. After much persistence, he finally sent me a screenshot of an “official confirmation email” stating that reimbursement was not possible—then completely ignored me.

This was infuriating.

This agent had been handling our claims for nearly two years, yet he had no understanding of my mother’s medical condition or the policy details. Looking back at how he initially pushed medical concierge services, it became clear that he cared more about personal financial incentives than genuinely helping clients with their insurance needs.

Was I expecting too much from an insurance agent? Admittedly, they are not medical professionals and cannot know everything. It is understandable if he had never handled cancer claims himself. However, the real issue was his lack of initiative to verify information and his willingness to give misleading answers based on incorrect assumptions instead of seeking proper clarification for his client.

This time, I decided to take serious action.

🏥 Contacted the insurance company directly and filed a formal complaint

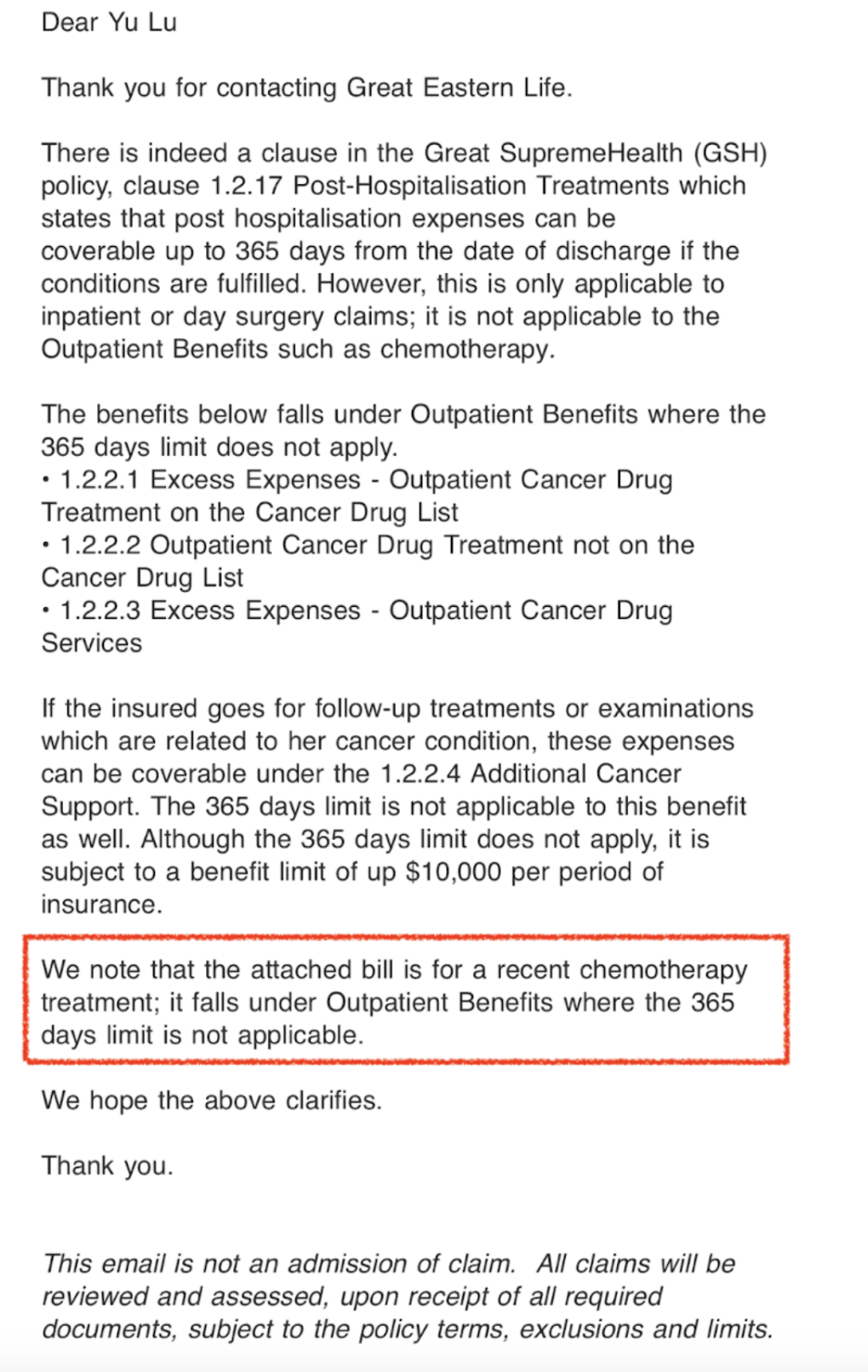

Doubting his response, I took it upon myself to verify the information. Faced with conflicting explanations, I decided to confirm everything directly. I spoke with official claims support to clarify the policy details over the phone. Their explanation aligned with my understanding:

- Chemotherapy and other cancer treatments could be reimbursed under outpatient cancer drug treatment.

- Consultations, lab tests, and scans were covered under outpatient cancer drug services.

- Neither category had a one-year hospitalisation restriction

After the call, I requested written confirmation via email, which they provided. I then filed a formal complaint with the insurance company:

- I demanded an explanation for the policy discrepancies and requested an investigation into the source of my agent’s “official confirmation.”

- I explicitly asked for my case to be handled under MAS’s complaints resolution framework, warning that otherwise I would escalate the matter directly to MAS.

Timeline of Formal Complaint and Insurance Company Handling

After filing a formal complaint, here is the timeline of how the insurance company handled the case.

🏥 Insurance complaint handling timeline

📅 Aug 17, 2024 – Filed a formal complaint with the insurance company.

📅 Aug 20, 2024 – Claims department acknowledged my complaint and said an investigation was underway.

📅 Aug 29, 2024 – Claims team called to clarify policy details.

He provided a full breakdown of my claims history and encouraged me to submit claims directly. When I asked about my complaint against the insurance agent, they said another department was handling it but could not provide updates.

–One month of complete silence–

📅 Sep 25, 2024 – The insurance agent suddenly contacted me to update me on the claim.

He had no idea that he had missed submitting an invoice, which I had already sent directly in early September instructed by the customer service. He then tried to mislead me by blaming the insurance company for slow processing, when in reality, he had forgotten to submit the claim. For the first time, I confronted him directly, making it clear that I knew he had provided completely incorrect policy information. He still did not acknowledge his mistake—whether he was genuinely unaware or simply pretending remains unclear.

📅 Sep 26, 2024 – Given my agent’s attitude, I no longer trusted that the insurer had conducted a proper investigation. I sent an email to follow up on the complaint’s progress.

📅 Sep 27, 2024 – A customer service representative called to pacify me.

I asked her, “Should I trust my insurance agent?”, “Is it his responsibility to process claims?” and “Is he accountable for providing incorrect policy information?” Her answers were ambiguous, and she could not give a definitive response. She promised an update by October 2.

📅 Oct 2, 2024 – No response. I called customer service but could not reach anyone.

📅 Oct 11, 2024 – Received an email stating that my complaint had been escalated to the insurer’s compliance department and that the insurance agent would be investigated. Due to confidentiality policies, they could no longer provide further updates (which is standard under MAS regulations).

📅 Oct 24, 2024 – Given my continued distrust of the insurance company, I officially escalated the complaint to MAS to ensure oversight of the investigation. I also raised concerns about how frequent changes in insurance policies make it difficult for insurance agents to maintain accurate and up-to-date knowledge.

–Three months of complete silence–

🏥 Final Response from insurance company

📅 Feb 06, 2025 – I finally received the insurance company’s investigation outcome regarding my complaint.

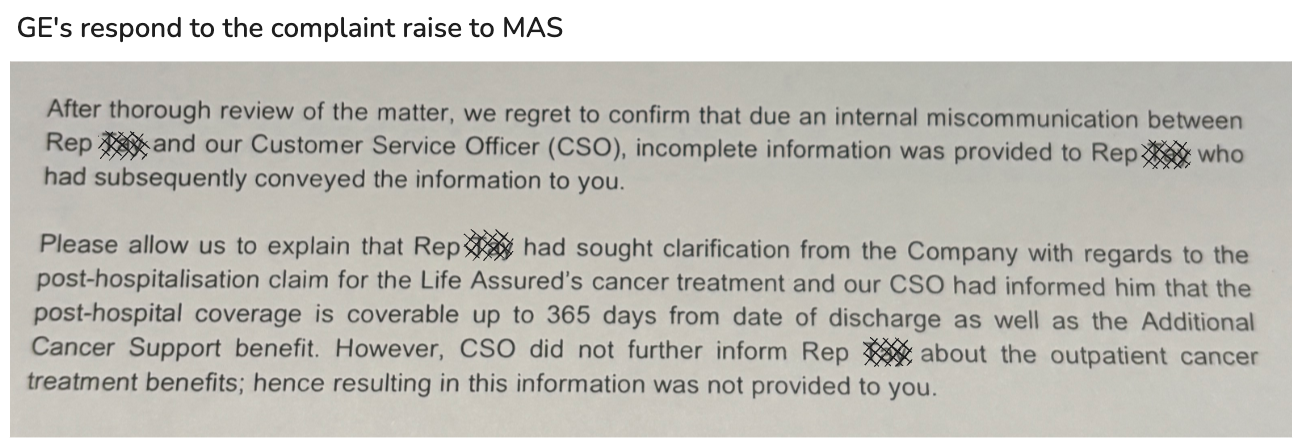

They did not acknowledge any negligence on the part of the insurance agent. Their explanation was that when the agent consulted internal staff about the policy terms, he only asked about pre-/post-hospitalisation coverage. The internal staff did not provide information on cancer treatment coverage, which resulted in the agent not conveying this information to me. However, the actual situation was that I repeatedly emphasised and explicitly asked whether outpatient cancer treatment expenses (outpatient cancer drug list/services) were subject to a 365-day limit after discharge. The agent repeatedly and explicitly replied that such a limit did exist. This was not a case of insufficient information being provided to me, but of completely incorrect information being given.

If this had been another cancer patient unfamiliar with insurance policy terms and entirely reliant on the agent’s information, they might have surrendered their policy under the mistaken belief that insurance could no longer reimburse ongoing treatment. Later on, they would be even more likely to lose the best treatment opportunity because they could no longer afford the medication costs. I feel that continuing to argue with the insurance company is of limited value. After all, the agent’s negligence did not cause me direct financial loss. I hope they will take this issue seriously, ensure that insurance agents continuously learn and keep up with frequently changing hospitalisation insurance policy terms, and provide better support to clients. After all, if a so-called “financial advisor” has a fundamentally incorrect understanding of the product, how can they possibly help clients with proper financial planning? The insurance company also responded:

❝ We have since shared this case with the relevant teams, and the team members have been reminded of the importance of proper customer care, and the staff involved have been coached to address concerns raised by internal and external customers accurately ❞

Although this investigation outcome is disappointing, the small consolation is that the letter mentioned my case was shared internally. I hope that at least industry practitioners can learn from it and provide more accurate information to patients’ families in similar medical reimbursement cases—this is critically important to them. For me, what may be more meaningful is sharing this incident and my perspective from the standpoint of an ordinary consumer: a family member of a cancer patient, a risk-averse individual who has purchased multiple insurance policies, someone who has dealt with insurance company complaint and escalation departments more than once, who has read hospitalisation insurance policy terms multiple times in full, and who personally handled the entire process of organising and submitting hospitalisation insurance reimbursement documents for a family member—in the hope of helping those who need this information.

Final Thoughts

This experience made me reflect on the broader dynamics between MAS, insurance companies, insurance agents, and customers. I did not initially file my complaint directly with MAS because I understood how Singapore’s regulatory framework operates. MAS follows a principles-based approach, emphasising outcome-focused and shared-responsibility principles. It grants financial institutions, including insurance companies, considerable autonomy in setting internal policies. As a result, even when complaints are made to MAS, the first step is always for the insurance company to conduct an internal investigation.

This regulatory approach promotes market freedom, which is essential for a healthy financial market. However, because it is nearly impossible to establish universal “golden rules” governing financial practices, MAS relies on a range of tools—including guidelines, codes, and practice notes—to provide regulatory oversight. While some of these frameworks include ethical standards for insurance agents, they are advisory rather than legally enforceable.

My complaint timeline revealed how outcome-driven the insurance company was. They quickly clarified policy details and ensured my reimbursement was processed correctly. However, when it came to internal accountability—such as investigating my complaint against the insurance agent—they became slow, evasive, and reluctant to provide clear answers. When customer service advised me to submit claims directly rather than through my agent, I asked what the purpose of having an insurance agent was. They had no answer. When I asked who should be held accountable for providing incorrect policy explanations, they were similarly unable to respond.

This reflects the natural consequences of MAS’s regulatory framework. MAS grants autonomy to insurance companies, requiring them to self-regulate their agents. Insurance companies, in turn, balance compliance with profitability. While they incentivise sales, MAS imposes boundaries to prevent excessive misconduct. The challenge for consumers is that these boundaries are not always clear. This is why customer complaints play such a critical role. While a single complaint may not lead to systemic change, it provides MAS with valuable data points to assess regulatory gaps.

What frustrated me most about my insurance agent was how he repeatedly tried to mislead me into believing that the insurance company and I were adversaries, and that he was the only one advocating for my rights. He misrepresented the insurer as being slow in processing my claims, when in reality he had simply failed to submit the necessary documents. He also portrayed himself as indispensable, when in fact I was able to obtain accurate policy information from the insurer in a single phone call—while he had misled me for two months.

The truth is that insurance companies have a duty to monitor their agents, but they also have financial incentives to ensure agents maintain strong client relationships to drive sales. Every player in this system—MAS, insurance companies, and agents—is engaged in a game of competing interests.

Ultimately, this experience reinforced my belief that insurance agents who are primarily motivated by commissions will never truly prioritise their clients’ financial security. They fail to understand that

every policy they sell, every financial recommendation they give, and every claims service they provide carries immense weight.

For policyholders and their families, these decisions can mean the difference between financial stability and crisis, between receiving life-saving treatment and being unable to afford care. Some insurance agents fail to realise how critical policy accuracy is for families battling late-stage cancer. Financial affordability directly impacts the duration of treatment a patient can receive—it can significantly affect a patient’s chances of survival.

Read More

Low Risk Investments in Singapore

For long-term investments, what options should I consider for low-risk investments?

CPF LIFE Explained: FRS vs ERS and Which Plan Makes Sense

A practical guide to choosing between CPF LIFE FRS and ERS, and comparing the Basic, Standard, and Escalating plans. Learn how your total asset size and estate planning needs should influence your retirement decisions.