Most people may not pay much attention to this topic, and I sincerely hope you never have to experience these thoughts or face a battle with cancer yourself. However, I know that some cancer patients have followed me because of my previous posts about cancer treatment and insurance reimbursement. Some have reached out privately with advice, while others simply offer mutual encouragement. That’s why I feel it may be helpful to share some of my experiences, information, and perspectives — for those who might someday find themselves in need.

When fighting advanced cancer, sooner or later, you inevitably run into the issue of drug resistance to targeted therapies. Every time I discuss new treatment options with my doctor, financial affordability becomes an important part of the conversation. My doctor mentioned that ever since the Cancer Drug List (CDL) was introduced, planning treatment regimens for patients has become even more challenging.

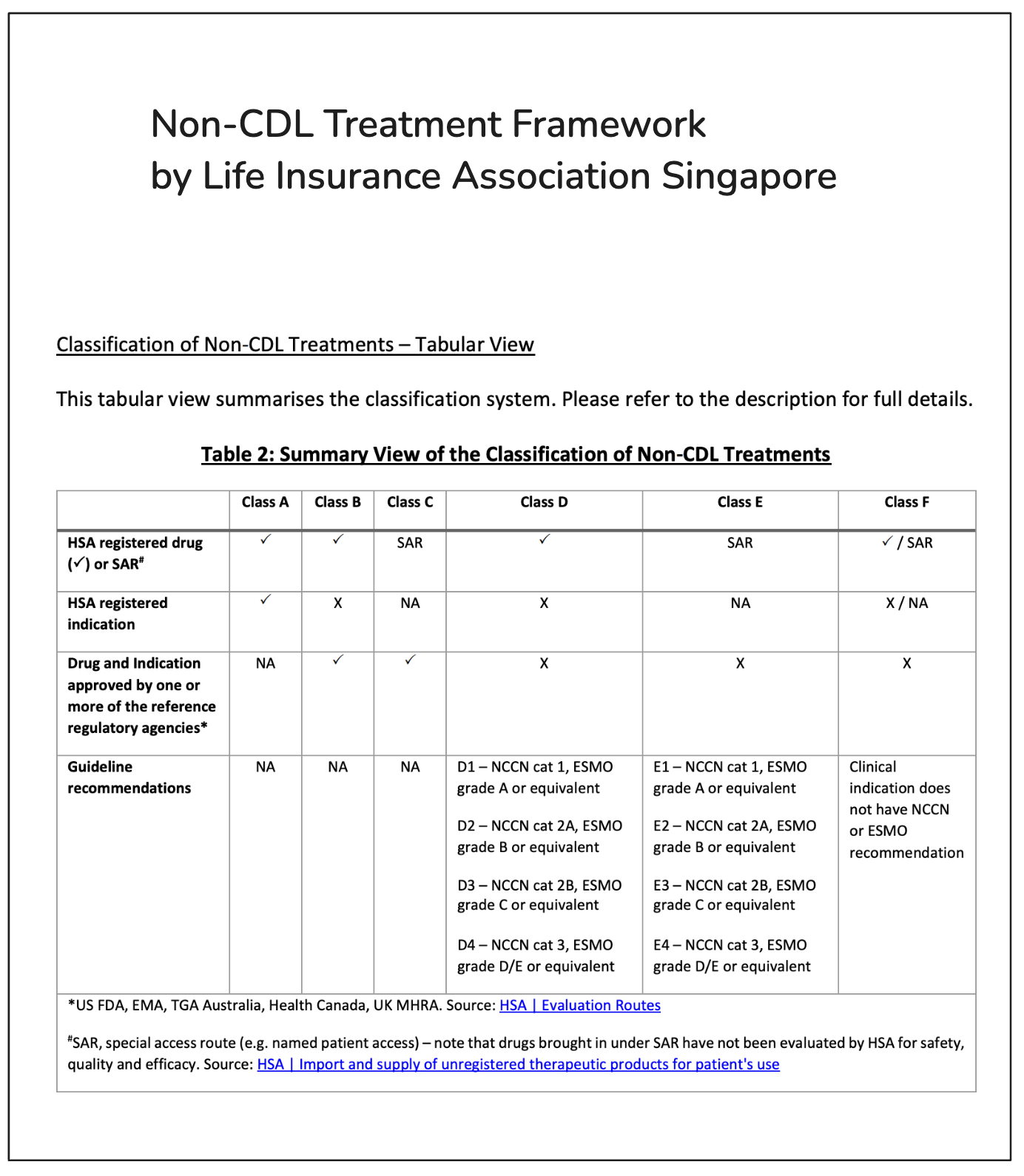

Only recently did I learn that beyond the CDL, there is also something called the Non-CDL Framework. This framework, introduced by the Life Insurance Association of Singapore, references various international cancer treatment guidelines and categorizes drug treatment plans into six tiers — from Level A to Level F. Most hospitalisation insurance riders cover part of the treatment costs for Levels A to E under the Non-CDL.

However, because definitions are complex and cancer treatment guidelines are constantly being updated, even doctors often aren’t certain which treatments are covered by insurance.

For instance, in our treatment plan, the genetic test report specifically recommended a certain drug. Yet because this drug was not listed for the particular rare cancer under the CDL, it wasn’t eligible for coverage — even though the drug itself is on the CDL for other types of cancer. The Non-CDL definitions were equally complicated. Despite the doctor’s repeated efforts to cross-check the cancer guidelines and find supporting references, even she couldn’t confidently predict how the insurer would assess it. All we could do was submit the application and wait to see how the insurance company would respond.

I also shared with my doctor some of the issues I faced during recent reimbursement claims. To be fair, part of the problem was on my side: when the resistance symptoms was developed, the doctor suspended the current targeted therapy prescription. I then submitted the PET-CT scan receipt separately without providing additional explanation. This led the insurance company to assume that the cancer treatment had ended and to reject the claim under the Cancer Drug Service clause.

Unfortunately, the way the insurance company’s customer service handled it afterwards was even more frustrating. Despite multiple calls and emails to explain and appeal, they seemed unwilling to seriously review the situation — as if they simply chose to “let the error stand.”

Our doctor also mentioned that many insurance admins aren’t truly familiar with policy details either. They simply follow standard procedures, and when a case becomes complicated, mistakes are easily made. Clinics, too, often find the insurance claims process tedious and time-consuming.

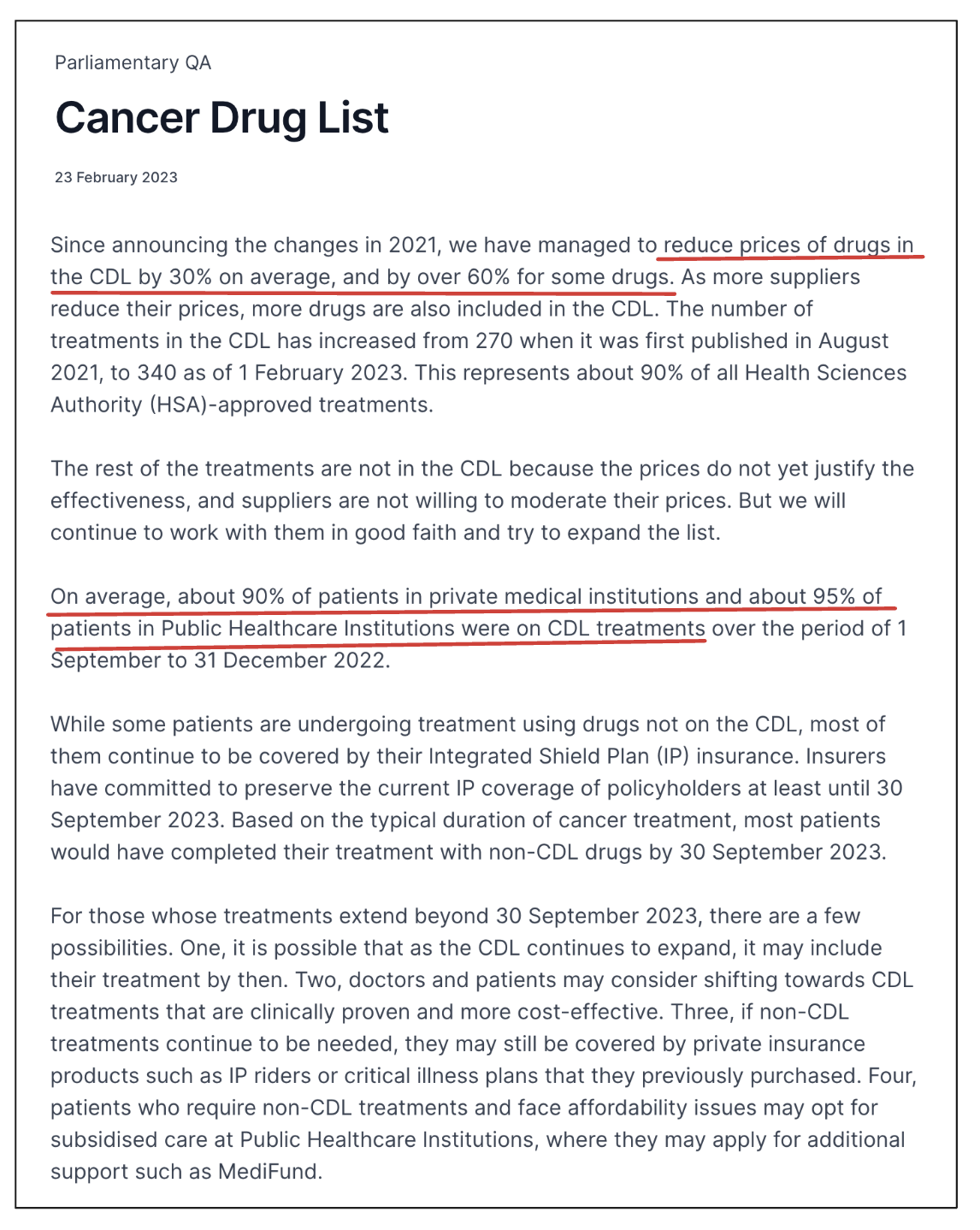

From a broader, national perspective, I do recognize the positive intentions behind the CDL policy. It has helped control escalating medical costs to some extent. In a 2023 parliamentary Q&A, it was noted that since the CDL was implemented in 2022, average drug costs have dropped by 30%, and 90% of private hospital patients and 95% of public hospital patients are now using drugs listed under the CDL.

But once these policies are applied to individual patients, it’s no longer about cost containment or statistical probabilities — it becomes about real people facing limited treatment options and bearing 100% of the high out-of-pocket costs. That’s the helpless reality.

I also understand that this is part of a larger push-and-pull between insurance companies and healthcare providers. There are indeed cases where both doctors and patients have abused insurance and medical resources, and some of these policies were designed to prevent such abuse. But they’ve also made things more complicated for doctors, who now face the difficult task of balancing treatment effectiveness with compliance to frameworks — all while trying to minimize the financial burden on their patients.

Perhaps we were simply unlucky to encounter some unreliable insurance agents. Most of the doctors we’ve worked with have demonstrated strong medical ethics — though I won’t deny that exceptions exist in both professions.