Should You Choose FRS or ERS for CPF LIFE?

I have always been a supporter of CPF and have actively topped up my SA and MA.

Previously, I conducted an in-depth analysis of retirement passive income planning. One of my key conclusions was that CPF LIFE is, in my view, the optimal retirement investment tool. It addresses several major risks in retirement planning: longevity risk, investment risk, and overspending risk. The low maintenance cost and stability of the CPF LIFE annuity are advantages that other investment channels cannot replicate, making it the most suitable source of passive cash flow for very elderly individuals.

So, should we automatically choose to commit to CPF LIFE ERS to receive the highest possible lifelong payout?

Not necessarily. This is not about return rates—because as discussed in the previous article, investment returns are not the most important factor in retirement planning. Rather, it relates to two other limitations of CPF LIFE: liquidity and policy risk.

A very important decision criterion is: what is your total asset size?

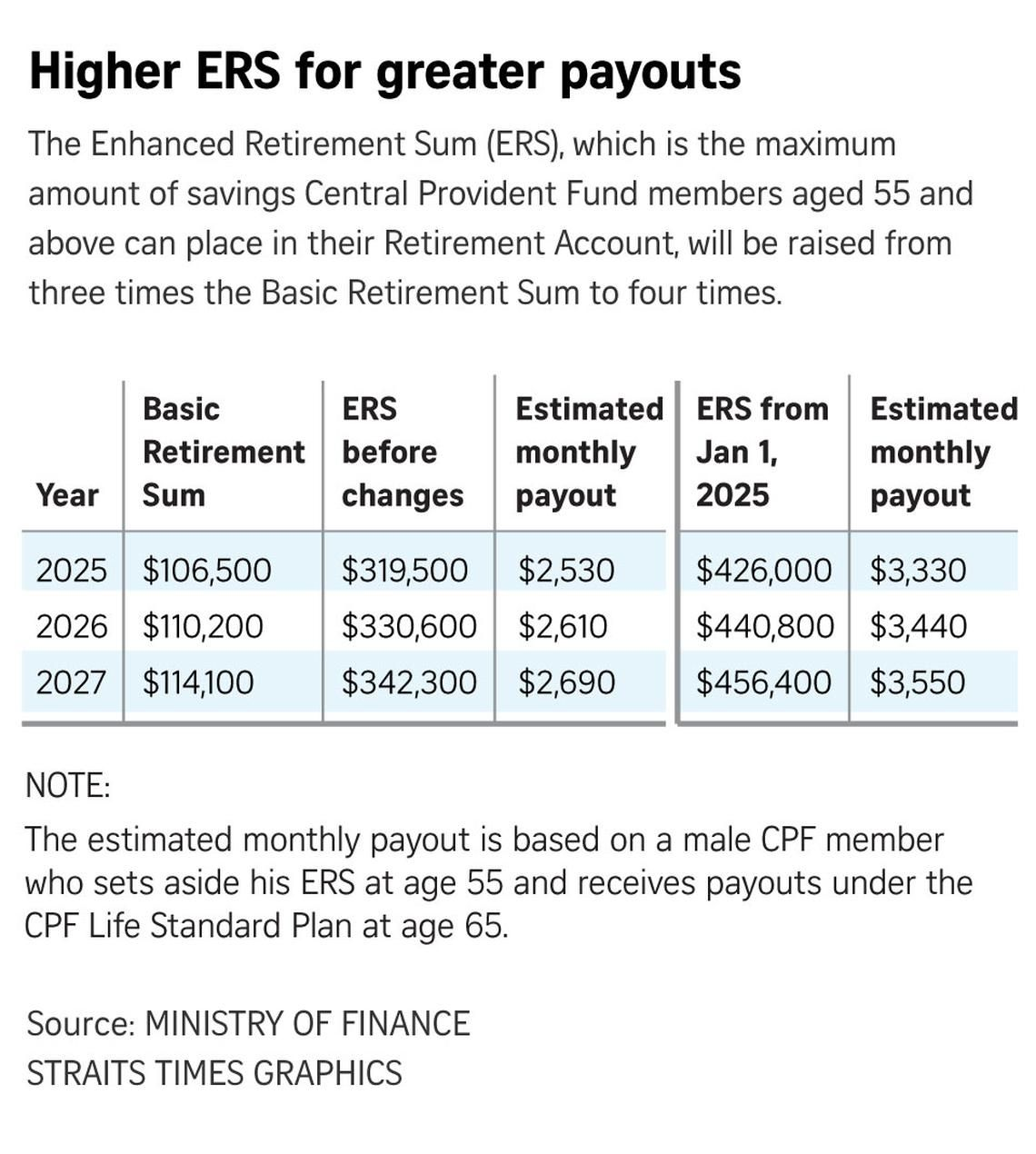

Currently, the CPF LIFE ERS is 426,000. Let’s use this figure as a reference.

Assume that at retirement you have more than 2M in total assets (excluding your primary residence), including CPF. Allocating 426,000 into an annuity is not a major issue. After all, it locks in a relatively sufficient lifelong cash flow. The remaining three-quarters or more of your assets can then be invested through other channels to diversify risk, enhance returns, maintain liquidity, and support additional estate planning.

However, if you retire with only 500K in total assets, choosing ERS would mean almost all your principal is locked into the illiquid CPF annuity scheme. In that case, the policy risk and liquidity risk you bear would be significantly higher. FRS (Full Retirement Sum) would be sufficient, leaving roughly half of your assets available for flexible planning.

What if your retirement assets are around 1M? It depends. Everyone’s risk tolerance, health condition, retirement lifestyle plans, and family responsibilities are different. Carefully analyze your financial situation, understand the underlying structure of financial products, and most importantly, know your life goals so you can plan your future accordingly. Only by considering all these factors can you make a better decision.

Data analysis keeps us rational, but financial decisions are not purely mathematical problems.

How to Choose a CPF LIFE Plan?

CPF currently offers three plans: Basic, Standard, and Escalating Plan.

These plans differ from the Full Retirement Sum (FRS) and Enhanced Retirement Sum (ERS) discussed earlier. The latter refers to the lump-sum amount committed, while the former refers to the payout structure in retirement.

According to the official guidance, the basic decision framework is:

- If you want steady payouts and do not mind inflation reducing your living standards, choose the Standard Plan.

- If you want to leave a larger bequest and also do not mind inflation reducing your living standards, choose the Basic Plan.

- If you want a steadily increasing cash flow to hedge against inflation, choose the Escalating Plan.

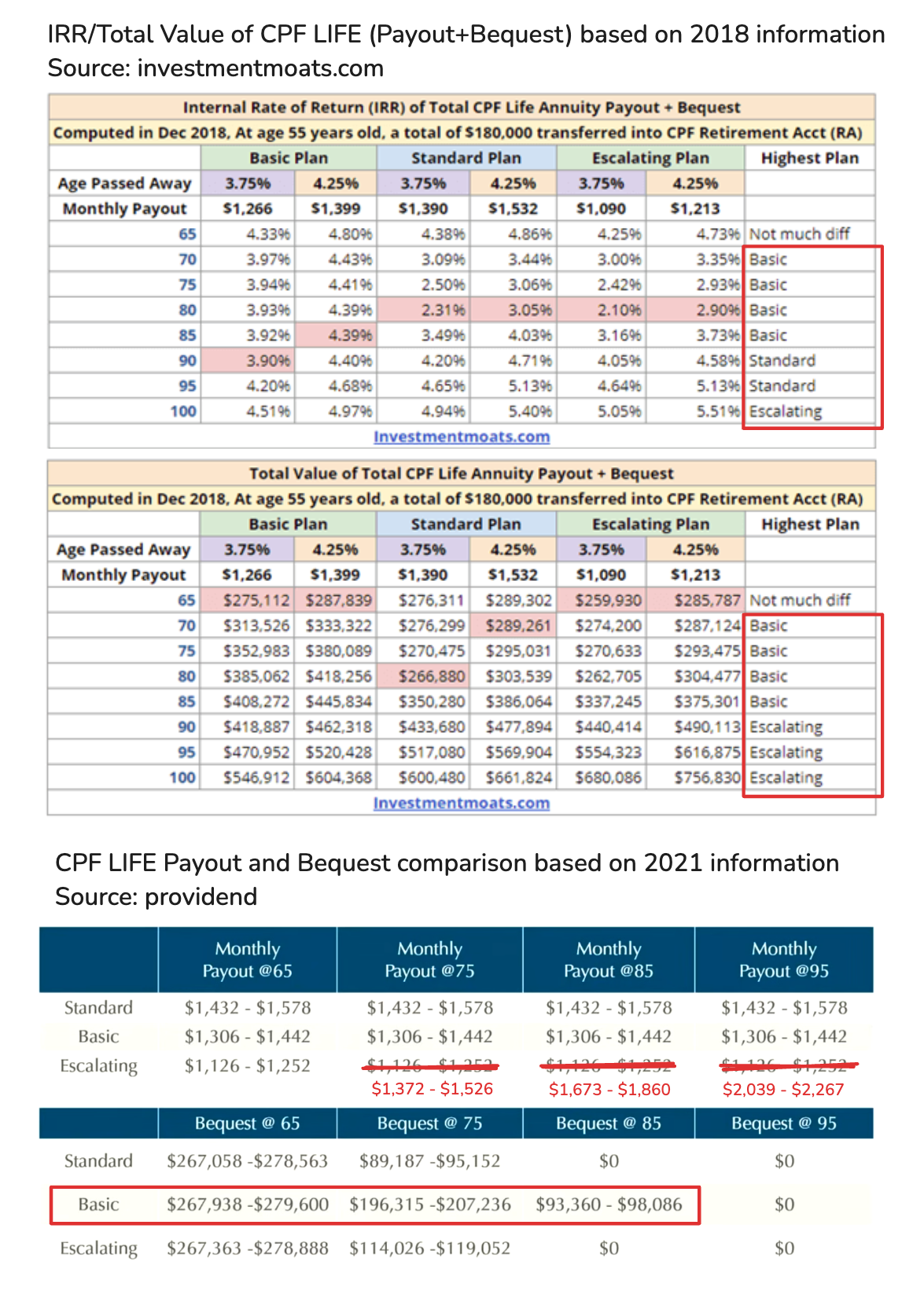

Of course, the decision is not that simple. Many analyses suggest that the Basic Plan may actually deliver higher returns. So what exactly are the structural differences between these three plans?

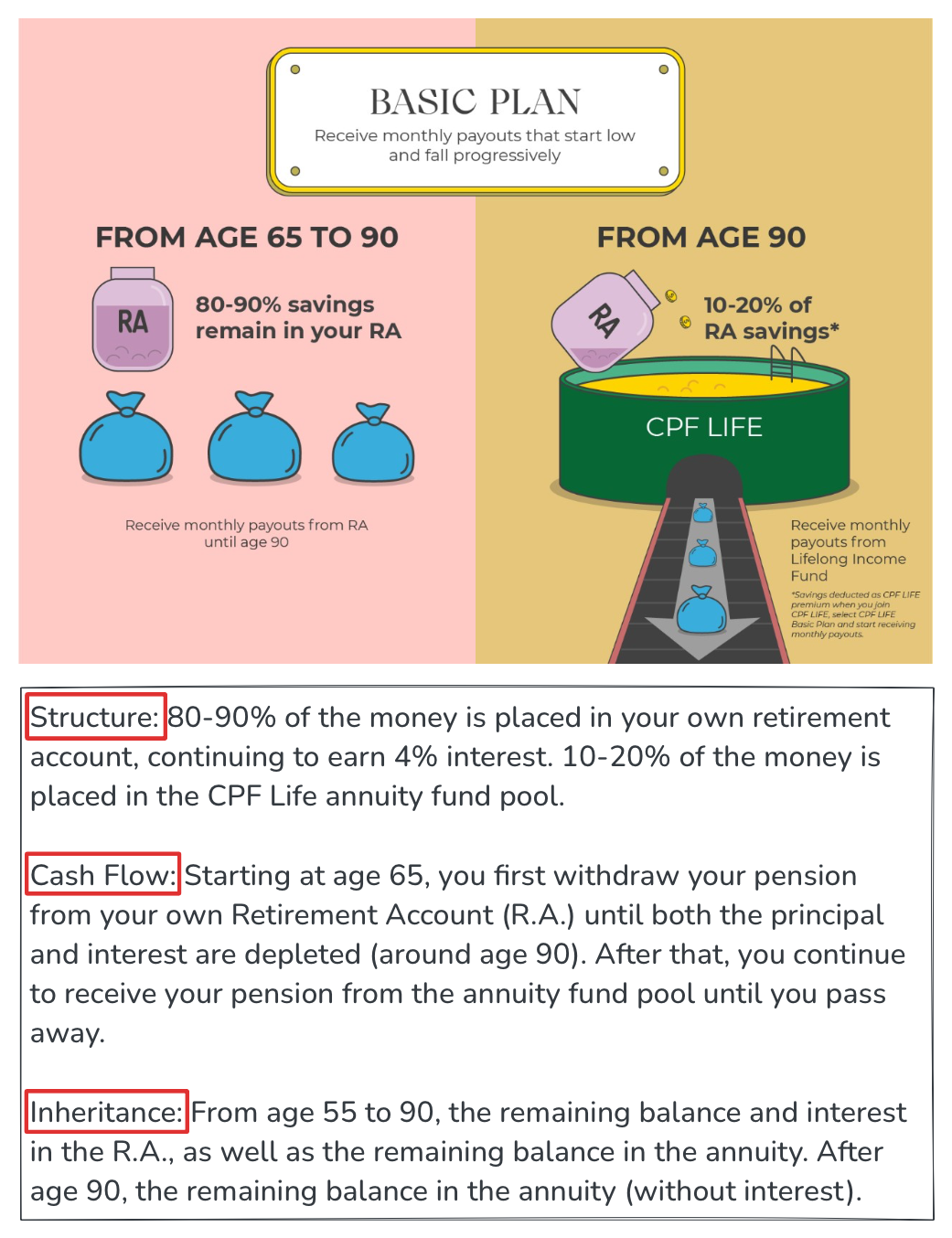

💰 Basic Plan: 80–90% R.A., 10–20% A.P.

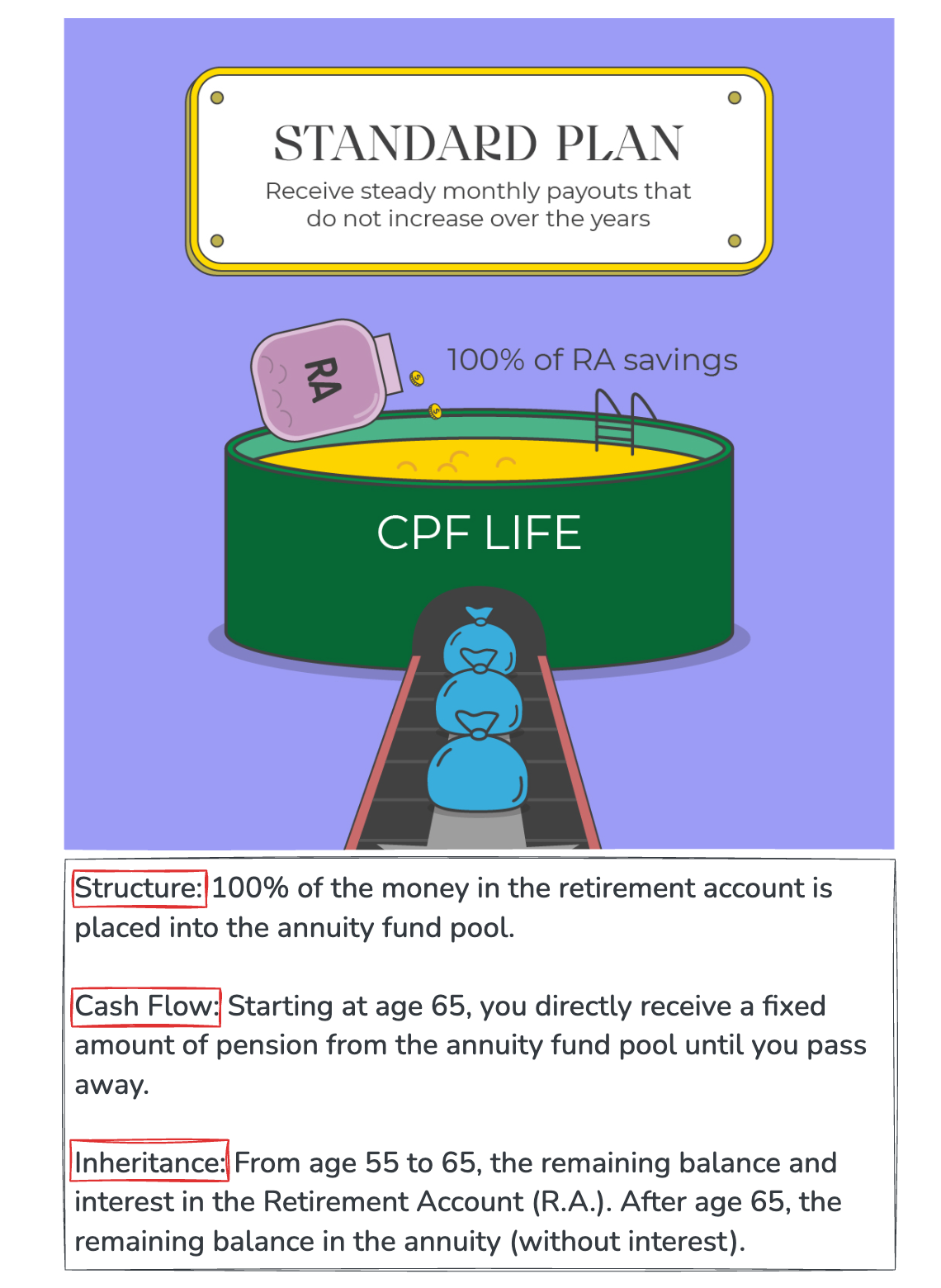

💰 Standard Plan: 100% A.P.

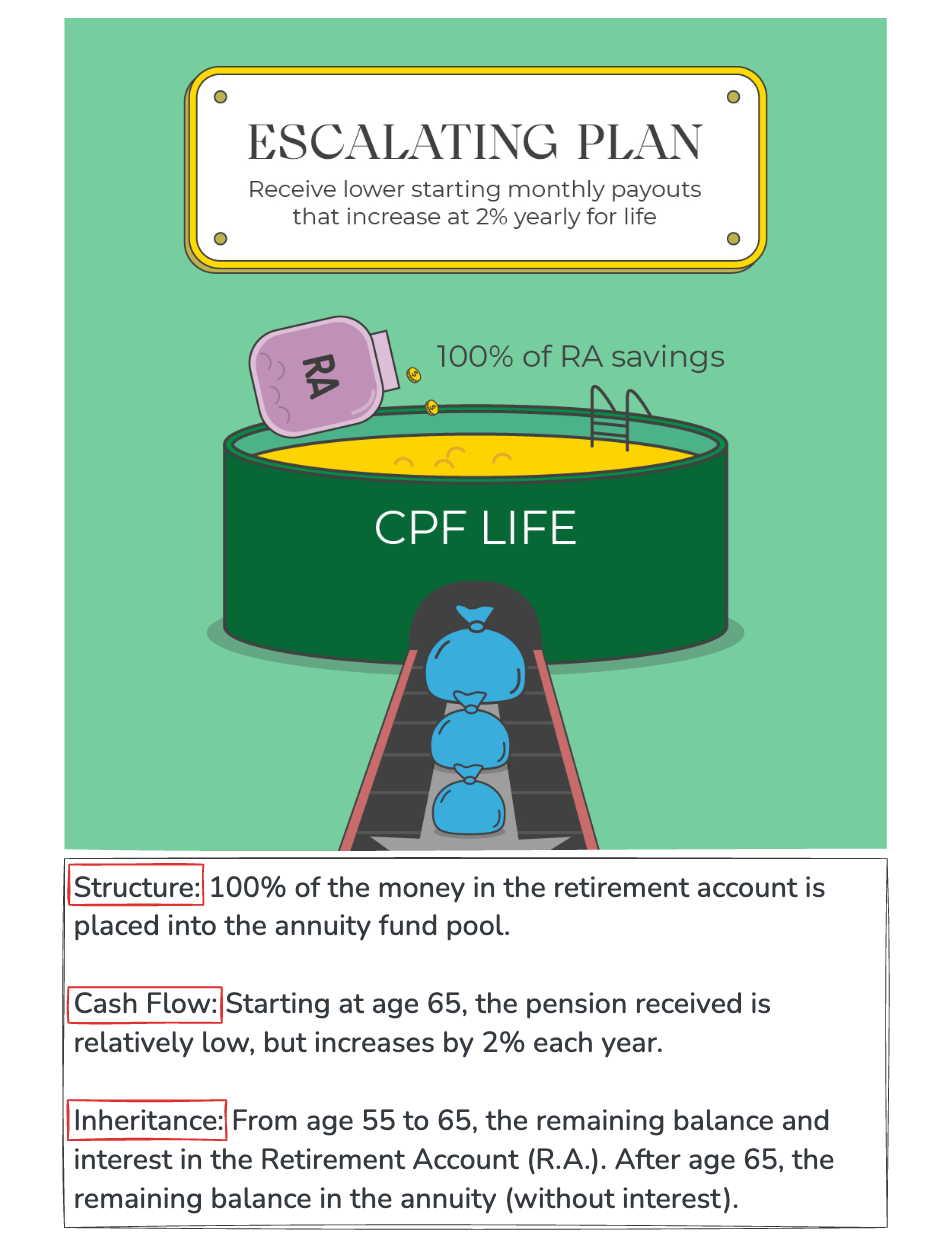

💰 Escalating Plan: 100% A.P.

Summary

The fundamental difference between the Basic Plan and the Standard/Escalating Plans is this:

Under the Basic Plan, most of the funds remain in the Retirement Account between ages 65 and 90, to be gradually withdrawn by the individual (this was essentially the structure before CPF LIFE was introduced), while a smaller portion is used to purchase an annuity to hedge against longevity risk.

Under the Standard and Escalating Plans, the full amount is used to purchase an annuity that begins lifelong payouts from age 65.

Because the Basic Plan contributes the least amount to the annuity risk pool, less of it is “pooled.” As a result, if someone passes away at a relatively younger age, they can leave behind a larger bequest. However, because less money is committed to the annuity pool, the later-life payouts are correspondingly lower.

Based on past calculations (the CPF website calculator no longer provides bequest estimates, so updated calculations are not available), and considering investment returns alongside average life expectancy, the Basic Plan appears to offer the highest returns.

However, if a person lives beyond 90 and continues receiving higher retirement payouts, the Standard and Escalating Plans gradually surpass the Basic Plan in returns—the longer you live, the more you gain.

When choosing an insurance product, probability always introduces uncertainty. Therefore, we cannot definitively determine which option yields the “highest return.”

I am still 20 to 30 years away from being eligible to receive CPF LIFE payouts. That is a long time, and policy changes during this period are unpredictable. From the government’s perspective, encouraging citizens to commit 100% into the annuity pool reduces overall policy risk and gives more flexibility in managing resources to cope with rapid population aging. This trend can be observed in CPF’s official communications, product naming, and the removal of return-focused calculations from the CPF LIFE calculator. As a legacy extension of earlier policies, the Basic Plan could potentially be phased out in the future.

If I were to choose under the current framework, my decision logic would mirror my approach to FRS vs ERS:

- If I have no estate planning needs, I would choose the Standard or Escalating Plan to optimize retirement cash flow.

- If CPF represents only a small portion of my overall investments, and I have other diversified income sources, I would still maximize the advantages of CPF LIFE—prioritizing retirement cash flow and longevity risk mitigation—by choosing the Standard or Escalating Plan.

- Conversely, if CPF is my primary retirement or estate asset, I might choose the Basic Plan to pursue potentially higher returns, while still maintaining a safety net of income beyond age 90.

- As for choosing between the Standard and Escalating Plans, I do not have a definitive conclusion. From a return perspective, the Escalating Plan requires living close to age 90 to break even. However, from a risk-management standpoint, it best addresses longevity and inflation risks. If I have other high-quality passive income sources, I might choose the Escalating Plan—reducing CPF payouts in early retirement in exchange for higher, stable, risk-free income later. In a sense, paying for peace of mind. But this is still a developing thought.

References

Read More

My Approach to Family Insurance Planning

It's the time of the year that the annual renewal of some of my family insurance policies is needed. While organizing my family's insurance policies, I thought that since I've discussed various insurance topics, why not share my family's insurance principles and strategies directly. Here I am sharing how I plan my family's insurance, with some useful

IUL and Index Investment Comparision

Comparing downside-protected IUL investment logic with direct index investment and 40/60 portfolios: 25-year backtest of floor-cap strategies vs market.