Do You Still Need Personal Hospital Insurance If You Have Company Coverage?

As a hardcore risk-averse person, I’ve definitely made sure my family is fully covered. I’ve shared this story before about kids’ insurance: after I got laid off and lost the company-provided hospital coverage for my family, my FA strongly suggested I get hospital insurance for my son ASAP. Forty-five days after the policy kicked in, he was hospitalized for his second bout of Kawasaki disease.

Over the past two to three years of instability in the internet industry, I’ve personally gone through one layoff and have also witnessed at least two rounds of layoffs every year at my current company.

After my first layoff, one of the hottest topics in our ex-colleagues chat group was insurance. Some older colleagues, or those with pre-existing conditions and without local residency status, started seriously considering expensive global medical insurance. Someone even asked our former company’s global medical insurance provider for a quote — early 30s, SGD 7,000+ per year — which instantly scared a lot of people away.

After the most recent layoff at my current company, our big boss suddenly sent a Slack message to the whole team saying he wanted to discuss something non-work-related: he strongly recommended everyone buy personal hospital insurance. The reason? One colleague affected by the layoff didn’t have personal medical insurance, and their ongoing treatment had been severely impacted.

Reimbursement Order: Personal Hospital Insurance vs Company Group Insurance

So if you have both personal hospital insurance and company group insurance, how should claims actually work?

There’s no one-size-fits-all answer. Group insurance coverage and limits vary by company; hospitalizations can be emergency admissions or planned surgeries; and some cases require hefty deposits or pre-authorization.

In most situations, company group insurance should be used first. When hospitalization is needed, you can contact your company’s relevant department to coordinate with the insurer. Policy-wise, the rule is:

❝ When the same medical expense is covered by multiple insurance policies, the IP hospital plan only pays after other insurance (such as company group insurance) has paid first, acting as the last payer to cover the remaining eligible amount.❞

That said, in emergency admissions, dealing with company insurance can be quite cumbersome. In Singapore, hospitals automatically e-file personal IP hospital insurance for citizens and PRs. Hospital admins can see your personal IP policy, and the hospital coordinates directly with the insurer. In the end, you only need to pay the out-of-pocket portion — and if the amount isn’t large, CPF usually covers it. Since the hospital handles everything and there’s no cash outlay, it’s super convenient. Many people just go with e-filing and never think about it again.

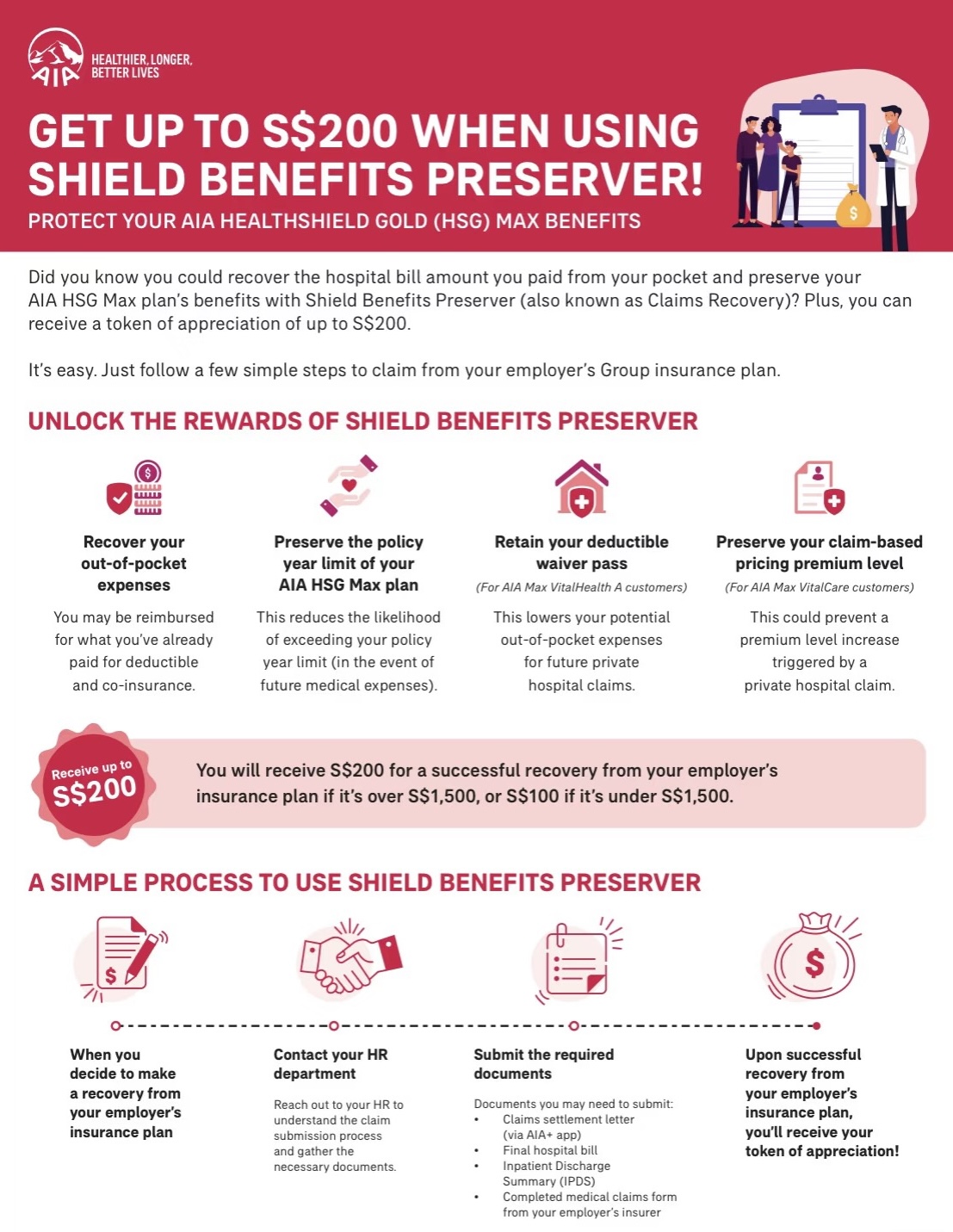

But here’s the thing: even if you claim through personal hospital insurance first, you can still apply for claims recovery from your company insurance later. IP insurers actually encourage this, since using group insurance helps reduce IP costs. AIA, for example, even offers cash incentives to encourage customers to apply for claims recovery after e-filing.

Personal experience here: I didn’t get AIA’s recover benefit somehow, though I did the claim recovery exactly follow their process. I am not sure if this is because my company insurance and personal insurance are both under AIA. Anyways, I didn’t follow up on this because this benefit was not the reason that I claim personal insurance first - I did that just out of convenience.

Claims recovery is beneficial for individuals too:

- Group insurance can cover out-of-pocket portions not covered by IP

- Group insurance can reimburse amounts paid by IP, restoring your IP coverage limits

- For IP plans where claims lead to premium increases or loss of benefits, restoring the reimbursed amount can also restore corresponding benefits

A Real Example and Why Claim Order Matters

I recently went through a claims recovery case myself. My two-month-old younger son had a fever and was hospitalized for two days. A few days after he was born, I had already informed HR to add him to our company’s group hospital insurance (which covers immediate family). About a month later, I also got him personal IP hospital insurance.

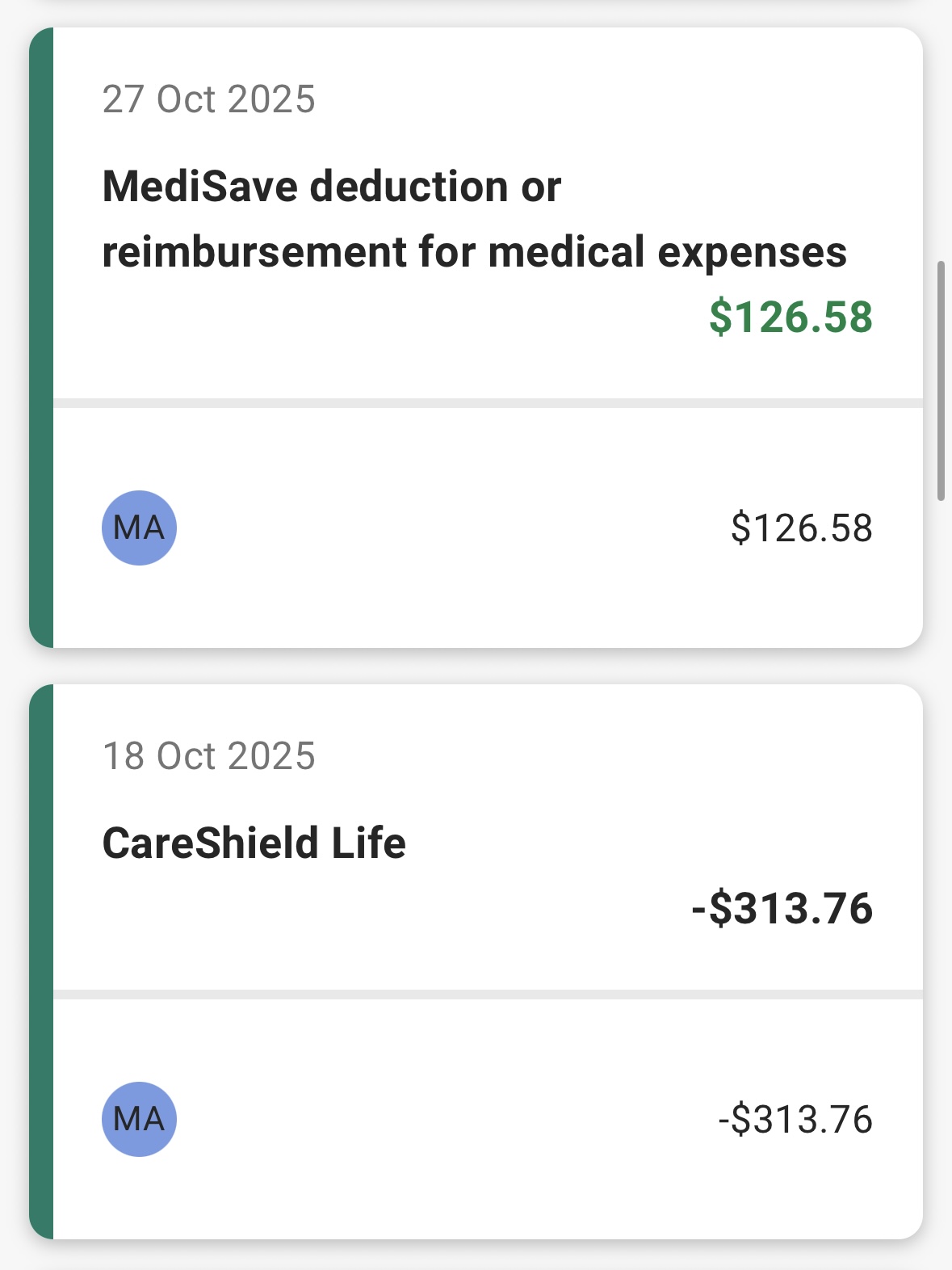

He was admitted in the middle of the night, and I wasn’t familiar with how company insurance worked, so I just went with e-filing through personal hospital insurance. From admission to discharge, we didn’t pay anything. A week later, the bill arrived: after insurance, there was a bit over SGD 100 out-of-pocket, which was paid via my CPF.

After that, I contacted the company group insurance customer service and uploaded the relevant documents through their online platform. About two weeks later, the group insurance processing was done: they refunded the CPF-paid amount and also reimbursed the IP insurer for the main policy payout.

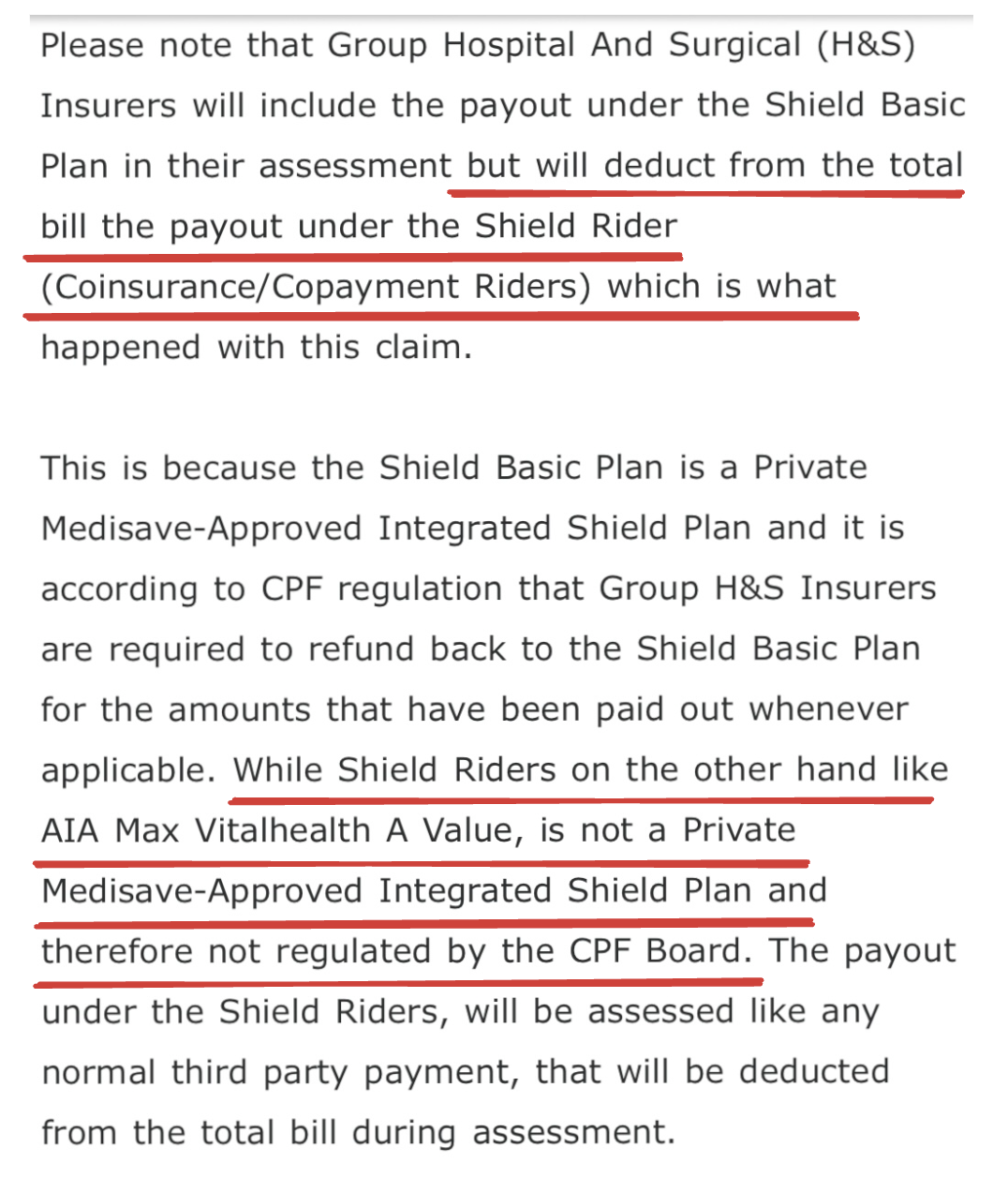

Customer service from AIA also explained an important detail to me: IP riders, since they’re not Medisave-approved, don’t have last-payer status. As a result, company group insurance won’t restore the portion covered by the rider — namely, the deductible, which can be several thousand dollars. So even with claims recovery, the order of reimbursement still matters. If group insurance is used first, neither the IP main policy nor the rider gets triggered. But if you use personal IP first and then apply for claims recovery, the portion paid by the rider won’t be restored.

So be cautious here, if you don’t want to touch your IP riders (probably due to concerns of raising premium after claim), claim your company insurance first! Because IP riders are not recoverable.

One more point in AIA’s favor (both my personal and company insurance are with AIA this time). After years of back-and-forth battles with GE, I’d gotten used to slow responses and messy processes from insurers. This time, the experience with AIA was smooth and efficient. When I reached out about group insurance reimbursement through internal company channels, I got timely and detailed replies. They’ve also recently integrated corporate and personal insurance platforms into a single app, making it easy to view all insurance policies for myself and my family — and submit claims directly in the app too.

Comparison: Company Insurance First vs Personal Insurance First

| Claim Company Insurance First | Claim Personal Insurance First (then recover) | |

|---|---|---|

| Convenience | ❌ More cumbersome, need to coordinate with HR/company | ✅ Hospitals auto e-file for citizens/PRs, no cash outlay |

| IP Main Policy | ✅ Not triggered, limits preserved | ⚠️ Triggered, but recoverable via claims recovery |

| IP Rider | ✅ Possibily not triggered, deductible untouched | ❌ Triggered and not recoverable |

| Premium Impact | ✅ No claims on IP = no premium increase risk | ⚠️ Claims may affect future premiums |

| Best for | Planned procedures, preserving rider benefits | Emergency admissions, convenience (remember to checkout if there’s cash incentives for claim recovery) |

Read More

Robert Shiller's Investment Philosophy

Shiller believes that people are inherently driven by incentives, willing to take risks, and selfish. Financial markets leverage people's self-interest to accelerate the flow of resources and increase social efficiency. Financial markets encourage risk-taking, and a healthy sense of risk and adventurous spirit is the source of innovation that drives the human civilization progresses. He encourages people to actively participate in the market and supports advanced financial products that enhance risk control and market freedom. Socialism is not the ideal scenario. Humans are complex, always evolving. A simple and ideal utopian world would deprive humans of the joy of invention and progress. Financial markets or the world are unlikely to become simpler, but with new inventions, they are becoming better and more interesting. He also constantly emphasizes the market turbulence caused by human factors, noting that greed sometimes drives financial markets to extreme madness, for which the participants ultimately have to pay the price.

Government Benefits for Familities with Newborns (2025)

Comprehensive guide to Singapore's baby bonus, MediSave grants, parental leave reimbursements, preschool subsidies, and tax reliefs for newborns in 2025.