As 2025 draws to a close, it’s a natural moment to look back on the year behind us and think ahead to what’s next. When it comes to personal finance, this annual reflection is more than a routine check-in—it’s a powerful habit that helps build long-term wealth and keeps life goals within reach.

My investment approach is firmly rooted in passive investing. I don’t chase excess returns, so my performance largely mirrors the broader market. Because of that, any single year’s return—good or bad—doesn’t carry much meaning on its own.

Instead of setting short-term return targets, I focus on savings goals tied to long-term investment objectives. Each year, I adjust my cash position, liabilities, and portfolio allocation to stay aligned with those goals rather than reacting to market noise.

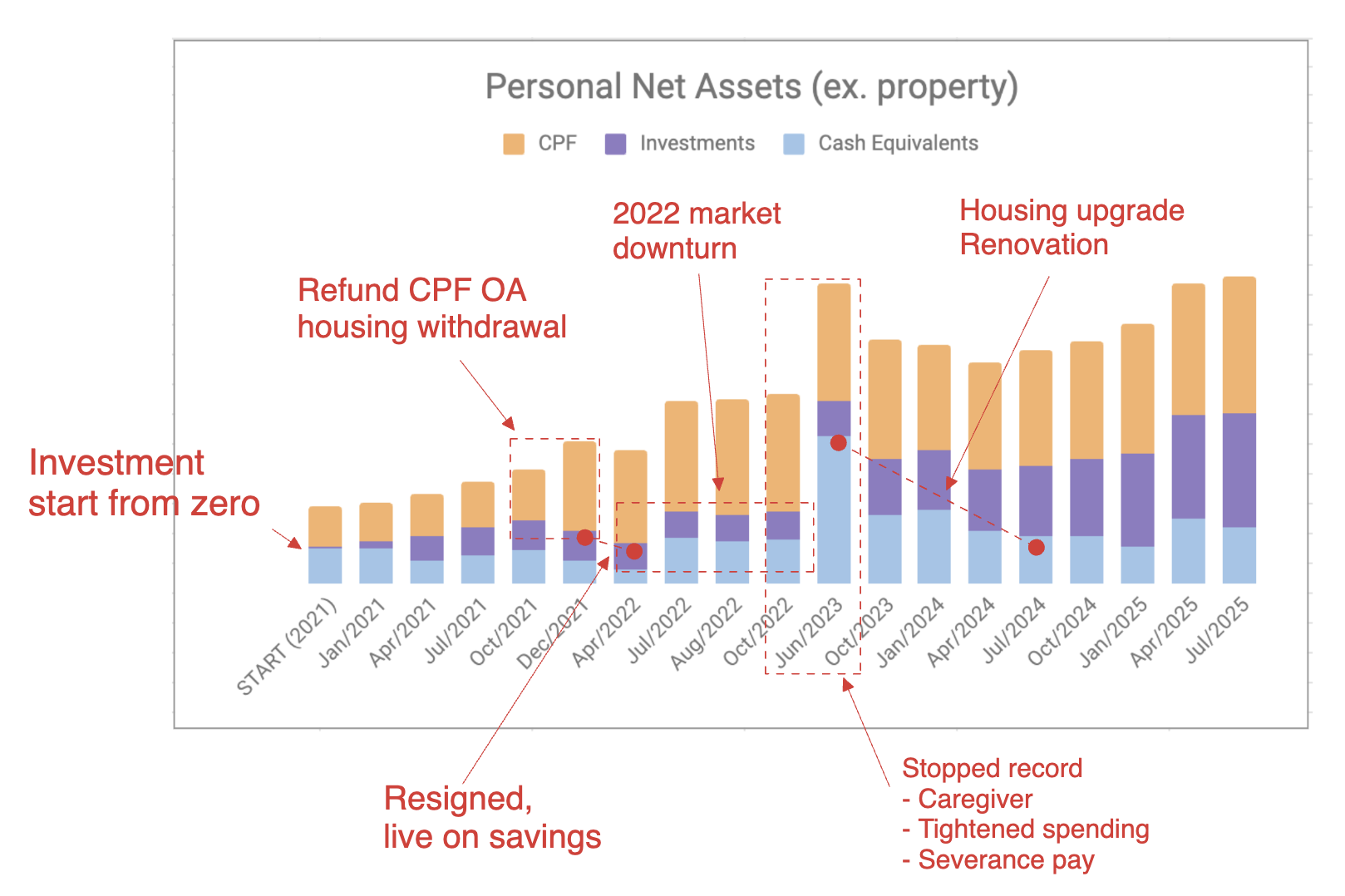

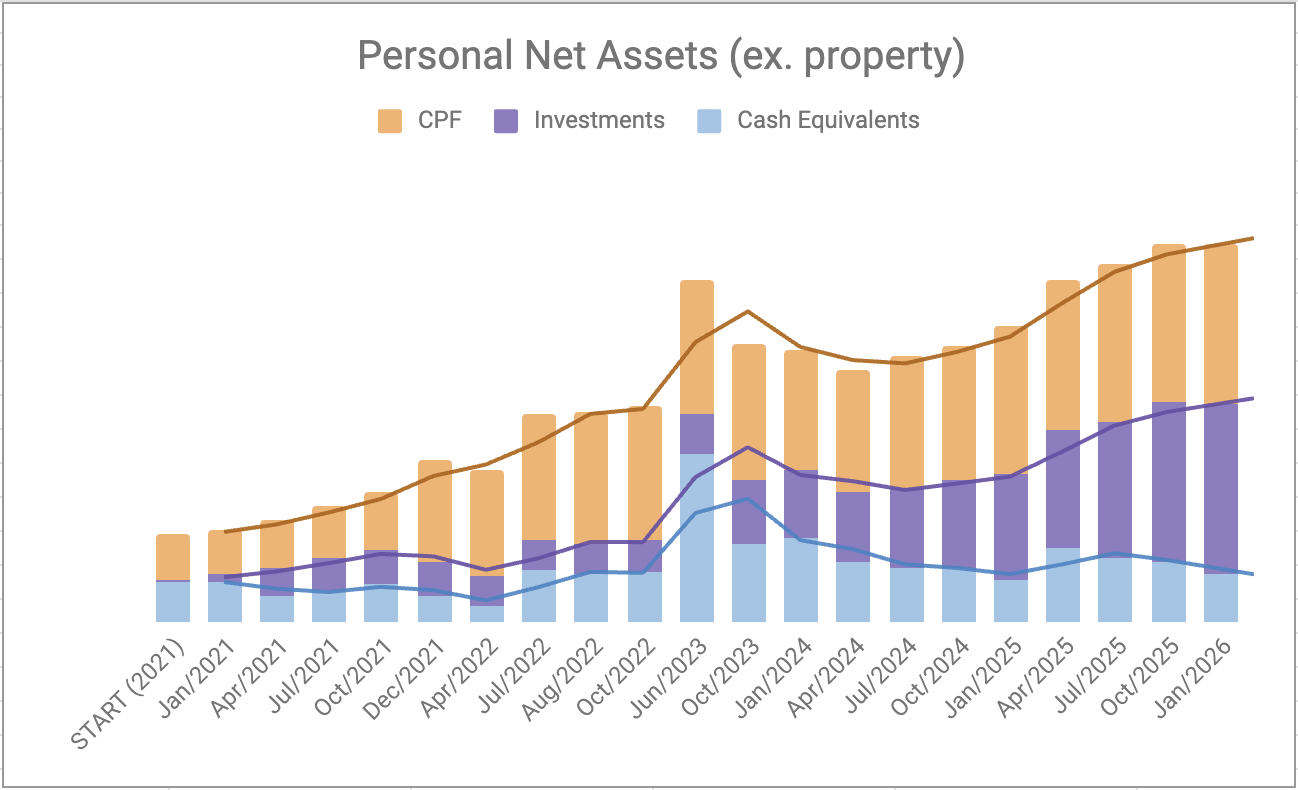

2021–2023: Reflection and Course Correction

When I reviewed my net worth changes from 2021 to 2023, a few weaknesses became clear:

- Financial asset accumulation was slower than expected

- Cash and low-risk investments made up too large a share of assets

- Large cash inflows weren’t invested promptly

- Owner-occupied real estate dominated total assets

- The financial market downturn in 2022 coincided with a surge in real estate

- Overall debt levels were relatively high

In response, I set a three-year investment and wealth management plan for 2024–2026. After several steady years of execution, I’m happy to say that most of these goals were already achieved by 2025:

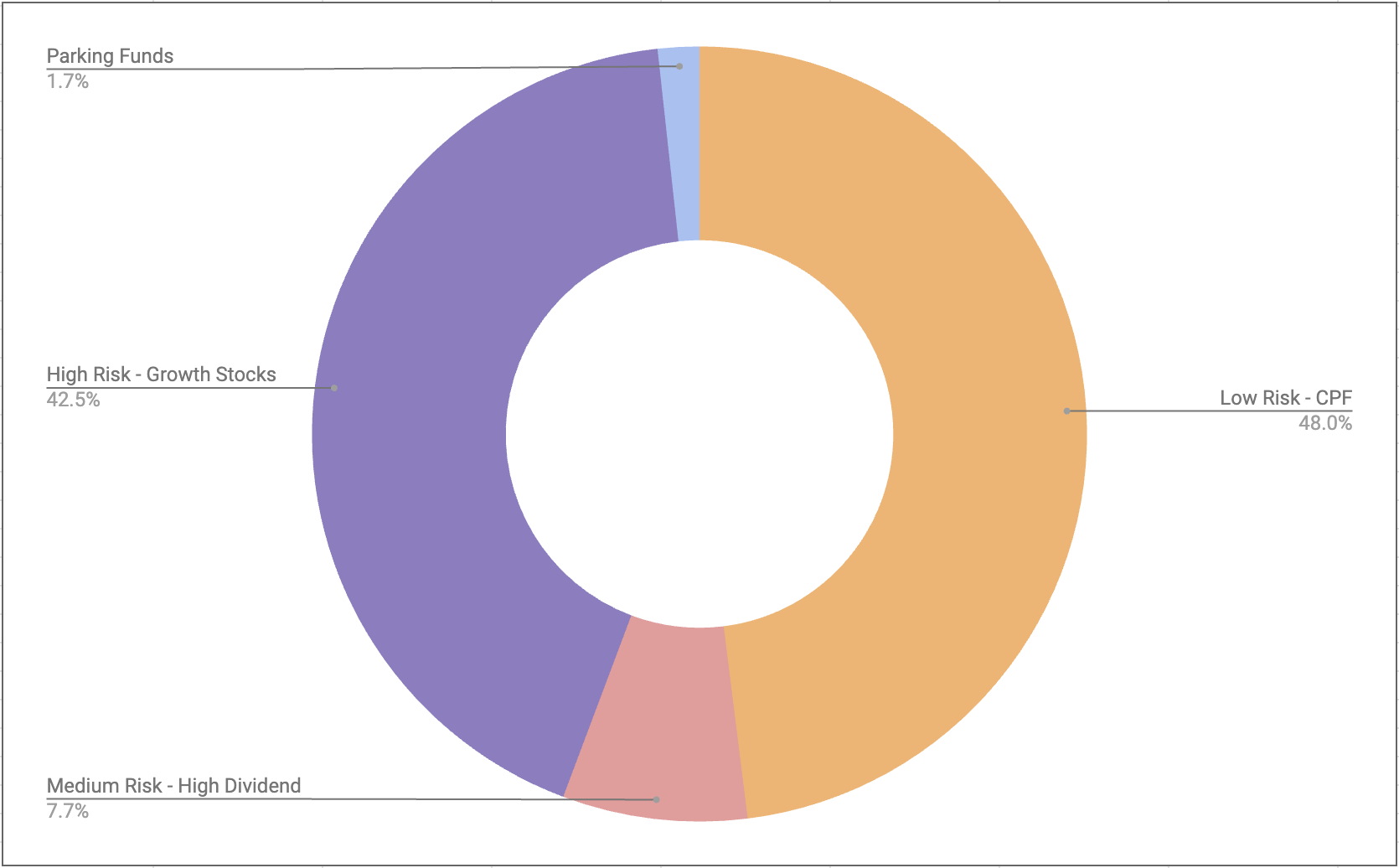

- Savings rate above 50% 👌🏻

- Stock-to-bond ratio above 40% 👌🏻 (25% → 52%)

- Debt ratio below 35% 👌🏻 (42% → 35%)

- Real estate below 50% of total assets 👌🏻 (60% → 45%)

These improvements didn’t come from dramatic changes, but from consistent, disciplined decisions made year after year.

New Year Resolutions for 2026

This year also brought a major life change—we welcomed a new family member. With higher expenses on the horizon, I plan to track spending more closely for a period of time to build more accurate budgets and set a realistic savings rate. As a result, my target savings rate has been adjusted slightly downward.

On the investment side, I’ll continue increasing exposure to higher-risk assets and gradually raise my stock-to-bond ratio. I also plan to introduce a small allocation to cryptocurrency. After reviewing my asset allocation and long-term goals, ChatGPT suggested keeping this exposure below 5%, which aligns well with my risk tolerance.

My 2026 Investment & Wealth Management Goals:

- Track expenses in greater detail

- Allocate less than 5% to cryptocurrency

- Increase emergency fund savings (partially via money market funds)

- Maintain a savings rate above 40%; save 50% of additional income

- Raise the stock-to-bond ratio above 55%

- Reduce the debt ratio below 30%

Happy saving, happy investing—and most importantly, happy living.

Read More

Our Renovation Journey: Budgeting and Quotation Cost Breakdown

Our S$70K renovation budget planning. Comparing 5 different IDs' quotations

Profoundly Simple Investment Strategies

Key investment theories from four finance legends: Markowitz's MPT, Sharpe's CAPM, Fama's EMH, and Bogle's CMH—and how they shape my portfolio.